Covered call writing trades have two legs: the long stock position and the short call, states Allan Ellman of The Blue Collar Investor.

The collar trade adds a third leg, the long protective put. The calculations for potential trade maximum gain or loss can be confusing. This article will break down the mathematics and provide a rationalization for these computations.

The Three Legs of the Collar Trade

- Buy a stock in 100 share increments (long stock position, a debit).

- Sell out-of-the-money (OTM) calls agreeing to sell our shares at a price higher than current market value (a credit and placing a ceiling on the trade).

- Buy OTM protective puts allowing us the sell our shares at a known lower price (a debit and placing a floor on the trade).

- The collar trade is structured such that the short call credit and long put debit results in a net option credit (the premium generated from selling the call > the cost of the long put).

Maximum Gain

This occurs when the price of the stock moves to or higher than the short call OTM strike. The maximum gain is realized when the profit earned from share appreciation of the stock moves from purchase price up to the OTM call strike. We then add in the net option credit to get the total dollar maximum return. The percentage return is calculated by dividing by the cost of the stock.

$ Max gain = (Call strike – Stock purchase price) + net option credit

% Max gain = $ Max gain/Purchase price of shares

Maximum Loss

This occurs when the price of the stock moves to or lower than the long put OTM strike. The maximum loss is realized when stock value moves from purchase price down to or lower than the OTM put strike. We then add in the net option credit to get the total dollar maximum loss. The percentage return is calculated by dividing by the cost of the stock.

$ Max loss = (Put strike – Stock purchase price) + net option credit

% Max loss = $ Max loss/Purchase price of shares

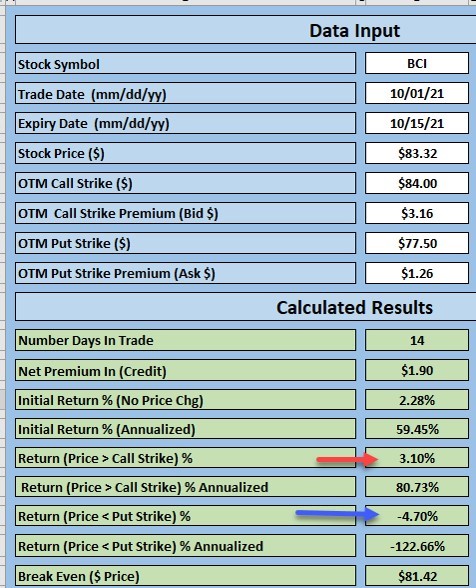

Hypothetical Example With the BCI Collar Calculator

Collar Calculations Using the BCI Collar Calculator

In the screenshot above, if BCI is purchased at $83.32 and the call strike is $84.00 (option credit of $3.16) while the put strike is $77.50 (option debit of $1.26), the calculations are as follows:

Max gain:

- Stock gain ($84.00 – $83.32) = $0.68

- Option net credit: ($3.16 – $1.26) = $1.90

- Net position ($0.68 + $1.90) = $2.58

- On a cost-basis of $83.32 = 3.10%

Max loss:

- Stock loss ($77.50 – 83.32) = -$5.82

- Option net credit: $1.90

- Net position: (-$5.82 + $1.90) = -$3.92

- On a cost-basis of $83.32 = -4.70%

Discussion

When calculating maximum gain or loss for our collar trades, we must have three data points:

- Net share gain or loss

- Net option credit

- Cost of shares

The initial trade structuring must result in a net option credit. The BCI Collar Calculator will do all the mathematical legwork for us.

Learn more about Alan Ellman on the Blue Collar Investor Website.