Most investors are focused on the war in Ukraine. Ultimately, a conflict in the South China Sea may be more important, suggests Jon Markman, editor of Strategic Advantage.

Chinese leaders revealed this past Friday that China will not impose financial sanctions on Russia in retaliation for the Ukraine invasion. The indifference makes sense given China’s military ambitions.

It should be a wake-up call for investors. Lighten up on Chinese stocks.

For decades the world’s democracies have cozied up to autocracies. The West trades access to billions of upscale consumers in exchange for resources and cheap labor. Russia extracted energy and metals, while China built the world’s factories. Politicians gambled that mutual prosperity would lead to shared peaceful interests.

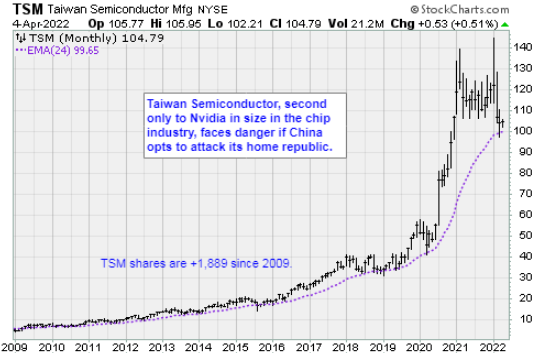

When Russia invaded Ukraine on February 24 the geopolitical calculus changed. Vladimir Putin saw an opportunity to grab a resource-rich country and further Russia’s status in the east. Xi Jinping, President of the People’s Republic of China, now sees an opportunity to reunify China with Taiwan, the semiconductor capital of the world.

Reunification isn’t well understood in the West.

Chinese leaders have never recognized Taiwan as an independent country. They see the island territory as a threat, and the roots of their concern run deep. Exiled Chinese leaders from the Ming Dynasty in 1683 used the island state as a base for attacks against the mainland. Meanwhile, Taiwan is a fortress, protected by 130 kilometers of treacherous waters and beachfront with clear line of sight against attackers. The hilly terrain provides perfect cover for armies and heavy weaponry.

The Chinese government threatened in 1995 to invade Taiwan. Thousands of Chinese troops massed in Fujian, the territory immediately across the Strait of Taiwan. The provocation was foiled only when President Clinton flooded the strait with American warships. War with Taiwan meant a larger conflict with the United States.

During the 40 years since that aggression China has been hardening its military. Its navy now outnumbers American vessels. The buildup in troops, tanks, helicopters, missile systems, and the PRC air force has been brisk, too.

Last October, those aircraft began to make almost daily flights though Taiwanese airspace. Although Taiwanese political leaders warned the flights were a violation of the aircraft identification zone, there has been no let up.

With the West now preoccupied with Russia, China has greater leverage to bring Taiwan back under its control, either diplomatically or through force. This is a problem for investors in Chinese stocks. The precedent has been set.

Within days of the Ukraine invasion, the Russian economy was effectively cancelled by the West. Large corporations pulled out. Mastercard (MA) and Visa (V) made it difficult for Russians to use credit. Coordinated Western economic sanctions stymied Russian banks. And the corporate keepers of the global stock indices removed Russian firms, making access to capital impossible. After tumultuous declines, Russian shares listed around the world simply stopped trading.

The Associated Press reported Friday that the official Chinese response to Russian sanctions is a flat “no.” China is opposed to choosing a side in the conflict. Officials are also unwilling to rule out providing Russia with financial and military aid.

Western corporations have limited access to Chinese consumers. Coordinated economic sanctions against China might also prove ineffective. However, delisting the largest Chinese publicly traded companies from world exchanges is doable. This process was set in motion last August after the Securities and Exchange Commission threated to delist hundreds of Chinese American Depositary Receipts (ADRs) for failure to abide by generally accepted accounting practices.

Investors should consider getting in front of en masse delisting by buying the ProShares Short FTSE China 50 (YXI). According to the fund fact sheet, the unleveraged exchange traded fund trades inverse to the daily performance of the China FTSE China 50 stock index.

At a current price of $16.65, the ProShares Short China 50 ETF trade significantly below the March 15 high at $22.70. That spike coincided with fears of greater Chinese regulation and the possibility the SEC may move ahead with delisting.

Shares could easily trade as high at $25 if tensions with China rise, a gain of 48% from current levels.