The Fed will be raising interest rates again soon, and of course, the question is whether the central bank will raise the Fed Funds rate by 0.75 or 1.00 percent, states Joe Duarte, editor of In the Money Options.

And if the recent inflation data—9.1% and 11.3% increases in consumer and producer prices for the month of June respectively—is any indication the odds favor that a symbolic 1% is on the table.

Some Fed speakers have denied that a 1% hike is likely, but no one knows what the central bank will actually do when it meets on 7/26-7/27. Still, the end result will be the same; the liquidity in the system will be reduced further, as the central bank began its QT tightening cycle by removing $50 billion worth of bonds from its balance sheet per month in June.

Unfortunately for the stock market, that $50 billion that the Fed will be disappearing, in one way or another, is money that won’t be available to banks like JP Morgan Chase (JPM), Morgan Stanley (MS), and Goldman Sachs (GS) for stock trading and related speculative activities.

It’s Personal for Mr. Dimon

The current effect of the Fed’s actions was pointed out by JP Morgan Chase CEO Jamie Dimon when after missing recent earnings expectations and watching his stock get clobbered (there goes the bonus) he noted: geopolitical tension, high inflation, waning consumer confidence, the uncertainty about how high rates have to go, and the never-before-seen quantitative tightening and their effects on global liquidity,” as reasons for his bank becoming so cautious that they will be raising reserves against loan defaults and halting their stock buyback program.

Moreover, details in his comments about why his company missed its earnings expectations by a fairly wide margin were interesting. Hint: it wasn’t that business was bad that caused the miss. It was the Fed’s recent stress test of Morgan’s balance sheet and the conclusion that JPM needed more money on the side in case of emergencies that prompted the increasing caution.

And that means that thanks to the Fed, a fact that Dimon openly complained about, Morgan now has less money with which to play around in the high-stakes derivative markets with trades that often affect overall stock market prices.

Certainly, that sounds like a lot of whining. But the truth is that if Morgan isn’t active in the markets that’s money that’s not creating liquidity for the rest of us, regardless of the focus of Dimon’s trades.

In other words, the Fed’s rate hikes hurt business for the big banks, and the liquidity drain that’s developing is a factor in the day-to-day volatility and stock prices.

Yes, that’s a big deal because if Morgan, Goldman, and Morgan Stanley trade less, then stocks fall. This results in 401 (k) plans, IRAs, trading, and crypto accounts taking a hit. And as familiar readers know, those four financial instruments are the backbone of the MELA system (M-markets, E-economy, L-life decisions, and A-artificial intelligence).

Indeed, when Morgan fails to trade, the market falls. And when the markets fall, the economy inevitably follows.

MELA Liquidity Crisis is Spreading—Now Hits Chinese Residential Market

Morgan’s liquidity issues are not exclusive. With global liquidity getting squeezed as stock markets fall, an interesting development was recently reported out of China, where an increasing number of people are refusing to pay their mortgages, a sign that the market’s liquidity squeeze is now moving into the real global economy.

At the center of the situation are falling property values resulting from the ongoing zero-Covid environment which is built around periodic shutdowns and other restrictions which in turn have led to unpredictable working conditions for factories and other businesses. The situation is threatening Chinese banks which are already grappling with liquidity stress among property developers, a fact that confirms, at least conceptually, Jamie Dimon’s expressed concerns above.

I recently discussed how liquidity and the MELA system (M-markets, E-economy, L–life decisions, A–artificial intelligence) are related and how they can be quantified by the Eurodollar Index (XED).

The relationship between stock prices and liquidity is built around interest rates. Generally speaking:

- Rising interest rates decrease liquidity

- Decreased liquidity increases bearish sentiment

- Rising bearish sentiment leads to falling stock prices

As the chart below shows, a fall in XED, caused by rising interest rates, leads to a rise in the CBOE Volatility Index (a rise in bearish sentiment which is illustrated by a rise in put option volume). The rise in put option volume then causes an increase in stock selling which pushes the price of the S&P 500 (SPX) lower.

Currently, it looks as if liquidity is no longer contracting, or contracting at a slower pace, which could explain why the S&P 500 is still above its recent bottom.

So, the real question is whether this is the proverbial “dead cat bounce,” or perhaps the start of what could be a significant bottoming process for stocks.

Currently, XED is fighting hard to remain above 97. A distinct failure at this price point could be very negative for stocks.

Watching Natural Gas as System Crash in Europe May be Unfolding

As if the issues in China weren’t enough, the festering Ukraine war-related energy-related issues in Europe could be headed for a major decision point, which is built around natural gas.

As things currently stand, Russia has cut off Germany’s natural gas supplies via the Nord Stream One pipeline for “scheduled maintenance.” The political situation in Ukraine is worsening and French president Macron is on the record as saying that Russia won’t likely turn the pipeline back on even if the mechanical issues are addressed. As a result, France is taking extreme measures to conserve energy, such as turning off street lights at night.

On Friday, Germany’s premier nat-gas seller Uniper announced that it may become insolvent if the German government doesn’t address the supply situation. Uniper also announced that it is now drawing on winter reserves to supply customers in the present.

Natural gas nearby futures responded by moving decidedly higher on 7/15/22, while the Natural Gas Index is trading in a tight pattern near its recent bottom right above its 200-day moving average. Constricting Bollinger Bands (green lines above and below prices) suggest that a big move in XNG is coming.

VIX Breaks Down. NYAD Carving Out Bottom

The NYAD Advance-Decline line (NYAD) continued its recent improvement as bearish sentiment continues to decrease.

There is no major advance in NYAD at the moment, but at least in the short term, the bearish lower high lower low trading pattern has been replaced by what looks to be a triple bottom. The next step, if a longer-lasting bullish trend is to reassert itself is a sustained move above the 50-day moving average.

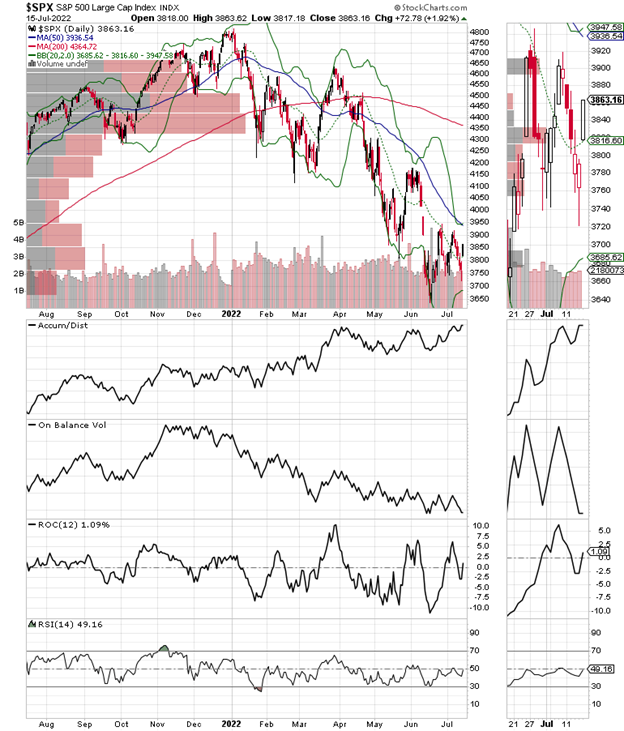

The S & P 500 (SPX) is also continuing what appears to be a bottoming process with short-term resistance at 3900 with room to run toward 4000 if the index can remain above 3900. Accumulation Distribution (ADI) is rising which means short covering is ongoing. A turn-up in On Balance Volume (OBV) would be very encouraging, as it would signal buyers coming in, but it has yet to materialize.

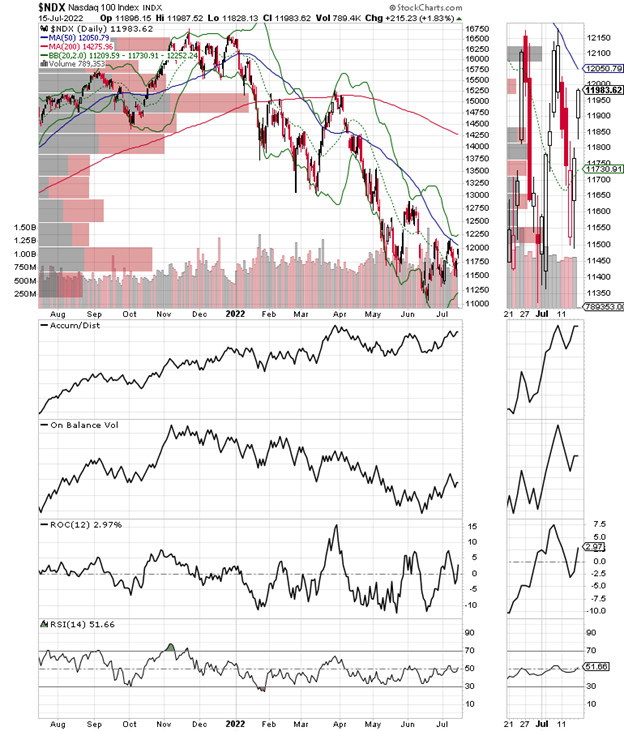

The Nasdaq 100 Index (NDX) has moved above its 20-day moving average and may have a fighting chance to move above the 50-day and the 12500 area if liquidity conditions improve. Accumulation Distribution (ADI) and On Balance Volume (OBV), are improving.

What comes next is clearly going to hinge on what happens if and when the major indexes reach and test the approaching resistance levels. And, of course, that will depend on the liquidity available in the market.

To learn more about Joe Duarte, please visit JoeDuarteintheMoneyOptions.com.