The US dollar traded higher during Easter Monday after finding some support on the back of Friday’s US non-farm payrolls report, states Fawad Razaqzada of Trading Candles.

But at the time of writing by Tuesday morning, most of those moves had unwound and the likes of the EUR/USD and GBP/USD were back at pre-NFP, while XAUUSD rose back above $2K and BTCUSD climbed north of $30K for the first time since last June. Investors will be looking forward to the release of some key data this week to provide fresh impetus for the FX majors. Thus, there’s a chance we will see continued range-bound activity until at least the middle of the week in the dollar before it establishes a clear directional bias.

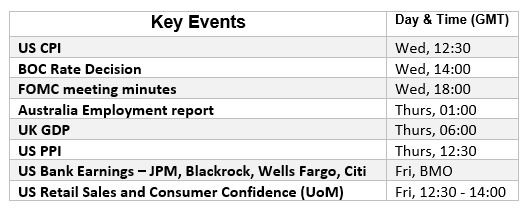

What Are the Key Events in FX Calendar This Week?

Out of all of this week’s macro events, Wednesday’s publication of the US Consumer Price Index is likely to be the most interesting one. Unless we see a much weaker CPI print, then this should make the case for a 25bp Fed hike on the third of May.

US CPI and FOMC minutes (Wednesday, April 12)

Thanks to weakness in US data, the market has been repricing lower than the Fed’s projected interest rate path in recent weeks, causing a significant downward move in the dollar. The market will continually question whether this is the right approach. So, a lot of attention will be on CPI as investors try to front-run the Fed. Headline CPI is expected to have fallen further to 5.2% year-over-year in March from 6.0% the month before. Core inflation is seen edging higher to 5.6% from 5.5% previously. There will be more inflation data on Thursday in the form of PPI. However, the latter is not going to be as important as the former.

The FOMC meeting minutes will be released later in the day, and they will reveal some of the Fed's thinking behind the 25bp hike in March, amidst the banking crisis. If the minutes reveal concrete signs that the central bank is very close to a peak in interest rates, or policymakers confirm to market expectation of cutting interest rates later in the year if needed, then this would likely be seen as dollar negative.

BOC Interest Rate Decision (Wednesday, April 12)

The Bank of Canada became among the first major central banks to pause its rate-hiking at its March meeting when it held interest rates unchanged at 4.50%. It is unlikely that the BOC will change its mind so soon after that pause. But the OPEC’s decision to sharply cut oil production may create fresh inflationary pressures and help improve Canada’s terms of trade given that the North American country is one of the top oil exporting nations in the world. So, there is a possibility that the BOC may sound more hawkish than expected, which may mean an even stronger CAD following its recent recovery.

US Retail Sales and UoM Consumer Confidence (Friday, April 14)

The Fed’s rate projections have been cut sharply in recent weeks owing to weakness in US data and signs of peak inflation. Worries over the health of US consumers will intensify if we see a weaker print in either retail sales or consumer confidence, especially as they are going to feel the impact of higher gasoline prices in light of OPEC’s decision to sharply cut crude production. Both headline and core retail sales are seen falling 0.4% month-over-month. The University of Michigan’s consumer confidence index is a more forward-looking indicator of consumer health and may thus trigger a sharper move in the dollar should we see a bigger-than-expected deviation from the expected 62.0 reading.

Dollar Index is Still in Downtrend

As the EUR/USD fell just shy of the 1.10 handle last week, this allowed the Dollar Index to bounce back to re-test key broken support from undeath at around 102.60ish. This level has now turned into resistance, with the index finding additional resistance from the 21-day exponential moving average.

Source: TradingView.com

Thus, the path of least resistance on the DXY continues to be to the downside until we see some higher highs or at least a clean break above the 21-day eMA. See the latest DXY chart.

Historically, the area around 103 has been pivotal in terms of creating the DXY chart here. Major turning points. The high of 2020 was formed at 103.00 while the peak in 2017 was made at 103.82. For as long as the dollar index holds below these levels, the dollar bears will remain happy. Only a move above these levels would see us turn tactically bullish on USD.

Therefore, as things stand, a move below the February low at 100.82 and towards 100.00 remains the more likely outcome from a purely technical point of view. This would imply the EUR/USD would most likely break above the 1.10 handle and GBP/USD above 1.25, US data permitting. A weaker inflation print on Wednesday could certainly get us to these levels.

To learn more about Fawad Razaqzada visit TradingCandles.com.