Though the GBP/USD has started the new week slightly on the back foot, there was some bullish price action observed towards the latter parts of last week, giving the bulls hope that it may be about to trend higher again. In truth, a lot will now depend on the direction of the US dollar, which will be heavily influenced by this week’s US CPI report, states Fawad Razaqzada of Trading Candles.

Greenback Bounces Back—For Now

Despite falling on Friday, the Dollar Index eked out a weekly gain to finish higher for the fourth consecutive week around the 102.00 handle. On Friday, a mixed US jobs report saw the probability of a rate hike in September fall to around 15% from about 20% before the data release. Correspondingly, the US Dollar Index and bond yields fell, gold rallied, and stocks stabilized somewhat, before resuming lower late in the day in the US session. However, some of those moves reversed in the first half of Monday’s session, with the GBP/USD and other major currency pairs turning lower, along with gold and silver. But it remains to be seen if there will be any further upside follow-through in the dollar buying.

With the July jobs report out of the way, there are now 3 more major data releases left for the market to weigh until the FOMC meets on September 20. Until then, we will have one more jobs report in September, and two more CPI reports—the first of which is due this Thursday. Any further weakening of CPI could cement expectations of a policy hold, and potentially weigh on the dollar.

What Will the Markets Focus On Next?

Investors will turn their attention toward consumer inflation data, due on Thursday. US CPI inflation has fallen sharply in recent times, printing below-forecast readings in each of the past 4 months. Annual CPI fell to just 3.0% in June from around 6.5% at the start of the year, increasing the likelihood that interest rates have now peaked.

But services inflation remains high as strong wage growth continues to push up input costs. This is something that was highlighted in the NFP report, which showed average hourly earnings rising 0.4% month-on-month or 4.4% year-on-year, which was more than expected. Annual earnings have now increased by 4.4% in April, May, June, and July. This shows that wage inflation is still going strong, and it is a concern for the Fed. This is especially the case for the services sector—which was also highlighted by the rise in the prices paid index of the ISM services PMI.

So, there is a risk that CPI could overshoot expectations on Thursday. But with the manufacturing sector clearly struggling, and now the jobs market softening a little, the Fed will feel that its policy is restrictive enough to help cool price pressures further. So, a small beat wouldn’t matter too much.

Economic Data Highlights for the Cable This Week

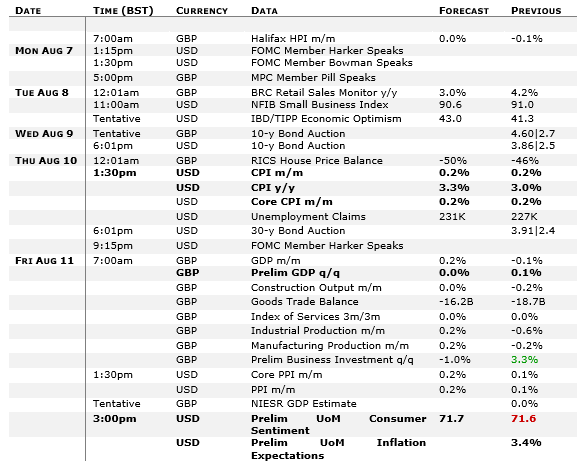

The economic calendar is not that busy this week, which points to a consolidation in the FX space. But we will still have at least two important data releases to look forward to from the US, which should impact all the dollar pairs, including the GBP/USD. From the UK, the main data releases will take place on the last day of the week.

US CPI

Thursday, August tenth

13:30 BST

US inflation has fallen sharply in recent times, printing below-forecast readings in each of the past four months. Annual CPI fell to just 3.0% in June from around 6.5% at the start of the year, increasing the likelihood that interest rates have now peaked. The Fed’s policy decision in September will be entirely data-dependent. Until then, we will have one more inflation report after this. Any further weakening of CPI could cement expectations of a policy hold.

US Consumer Sentiment (UoM)

Friday, August 11

15:00 BST

A Goldilocks outlook in the US is what stock market investors on Wall Street have enjoyed so far this year. They will be looking for signs that the health and sentiment of the consumer remain positive, enough not to increase the risks of a further Fed rate increase, and yet not too depressing to raise recession alarm bells. Somewhere in between could support stocks. FX investors will have already had the July jobs and inflation reports to consider along with the UoM consumer sentiment and inflation expectations surveys. If most of these indicators point to strength in the US economy, then this should keep the dollar supported on the dips.

UK GDP

Friday, August 11

07:00 BST

On Friday, we will have UK growth figures, as well as a handful of other macro indicators such as industrial production. Both the monthly and quarterly GDP estimates will be published. The Bank of England hiked rates further last week and warned more hikes could be on the way. One way for that not to happen is if the economy weakens more than expected, putting downward pressure on inflation. In fact, with mortgage rates surging, we have seen the housing market weaken. On Monday, we already saw the closely-watched Halifax HPI come in at -0.3% vs. 0% expected, adding to the 0.1% drop the month before. We will have the RICS House Price Balance on Thursday to provide more indications about the health of the UK housing market.

Here's the full economic calendar to watch, relevant to the GBP/USD pair:

What Else Has Supported the Greenback?

Last week’s earlier rally in the dollar had little to do with the Fed’s expected policy decision. It had a lot to do with the sell-off in the US bond market, especially at the long end of the curve. This was triggered by that rating downgrade by Fitch, causing investors to demand more for the increased risks associated with holding Treasurys. While a US debt default is unthinkable, it could happen at some future point in time. So, we wouldn’t rule out the possibility of further increases in US bond yields in the near term. It will be interesting to watch this week’s US bond auction (see calendar, above). This will tell us a lot about investors’ willingness to hold government debt.

That said, the correction potential for the dollar is now high, and investors have already started selling USD a little following Friday’s jobs report which come out somewhat on the weaker side with a headline print of 187K vs. 205K eyed and considering the fact there were downward revisions to the tune of 49K in the prior jobs reports. We also saw JOLTS report the fewest job openings in over two years earlier last week. But what is missing is some real downside follow-through for the dollar. Could that happen this week? CPI has the

GBP/USD Technical Analysis

The GBP/USD has pulled back to test support around the 1.2720 area – this being the head of the hammer that was formed on Thursday before we saw some upside follow-through on Friday. This level needs to hold on a daily closing basis to keep the bulls happy. But even if it doesn’t, and we see the cable drop a little lower from here, for as long as the June low at 1.2590ish doesn’t break decisively, so that the cable makes a lower low, there will be hope for the bulls.

On the upside, short-term resistance comes in around the 1.2780 to 1.2800 area. This was previously the support and is precisely where Friday’s rally stalled. A potential move above this area would give us a bullish signal, for then the cable would have also broken out of its short-term bearish channel.

To learn more about Fawad Razaqzada visit TradingCandles.com.