Refiners have historically seen upside as the energy cycle matures. In this case, we believe February’s record-setting cold snap has likely accelerated healing for the refiners by tightening the market and boosting crack spreads, suggests energy sector expert Elliott Gue, editor of Energy & Income Advisor.

Pure-play refiners don’t produce oil or natural gas and do not benefit from rising oil prices. These companies are best thought of as manufacturers that convert a raw material (crude oil) into a manufactured product (gasoline, diesel and jet fuel).

In fact, the ideal environment for refiners would be for relatively low oil prices in an environment where refined product demand is relatively tight.

As a result of both recovering demand and low US refinery production, inventories of gasoline have plummeted to 5-year seasonal lows.

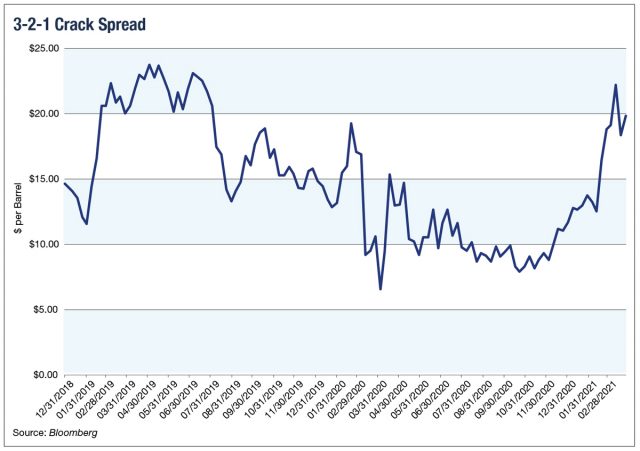

The 3-2-1 Crack Spread offers a good measure of US refinery profitability. It’s calculated by comparing the cost of 3 barrels of WTI crude oil to the value of 2 barrels of gasoline (84 gallons) and 1 barrel (42 gallons) of Ultra Low Sulfur Diesel (ULSD).

Take a look:

On this basis, refining profit margins have jumped from depressed levels under $10/bbl in late 2020 to the low to mid $20’s per barrel more recently. You can clearly see the big jump in refining margins starting around mid-February, which corresponds to peak refining outages and the resulting shortage of gasoline supply.

We believe this sets up a bullish scenario for the refiners this summer. That’s because demand for refined products looks poised for growth this summer as the coronavirus outbreak recedes, vaccines are widely rolled out and consumers take to the highways.

There could also be a pent-up demand effect as Americans who put off summertime travel and road trips in 2020 are particularly eager to emerge from lockdowns and hit the roads this summer.

At the same time, recent winter storms have pushed inventories of gasoline in particular to low levels at a time of year when demand traditionally picks up. In effect, crack spreads should rise into the summer months, providing a price signal for refiners to produce more gasoline and diesel to meet recovering demand.

Against that backdrop, we prefer refiners that exhibit two key characteristics. First, we prefer companies with refineries located along the Gulf Coast where they’re able to both access a wide slate of potential oil feedstocks and export markets.

And, second, we favor refiners that have strong cash flow sensitivity to refining margins because these companies will see the biggest boost from a potentially tight supply/demand balance into summer driving season.

With those points in mind, Valero Energy (VLO) remains our top pick in the group. Valero owns around 3.2 million bbl/day of refined product capacity with just under half that total in Texas, and an additional 16% on the Louisiana Gulf Coast. Thus, roughly two-thirds of total capacity is on the Gulf Coast.

In 2020, refining margins collapsed and there were some concerns about VLO’s ability to continue paying its $0.98 per quarter dividend. After all, the company’s total cash from operations was less than $1 billion in 2020 and the dividend works out to around $1.6 billion per year, resulting in an unsustainable shortfall.

However, the company is now through the worst of the downturn and should be in a position to cover and maintain its dividend going forward, so the risk of a dividend cut should recede.

Refining is cyclical business and current earnings are depressed by last year’s coronavirus-driven demand collapse, so we prefer to value Valero based on normalized mid-cycle earnings power of roughly $5.50 per share (that’s the consensus for 2023 earnings per share).

Applying a conservative multiple of 16 times those mid-cycle earnings, we see room for Valero to rally to $90+ per share this year, some 25% to 30% above the current quote.

Longer term, VLO’s investments in renewable diesel fuels — it’s already the largest producer of renewable fuels in the US — could both enhance growth prospects and improve the company’s ESG scores, leading to a higher valuation. The stock is a buy under $75