Historically speaking there are no bells rung at the start of a bear market. In fact, market tops are notoriously difficult to identify except in hindsight, as they are often quite volatile and take months to unfold, asserts Jim Stack, a "safety-first" money manager and editor of InvesTech Research.

While all market cycles are different, this is when a sound knowledge of market history can prove invaluable. As we’ve outlined in issues over the past year, the lofty levels of speculation and overvaluation, along with increasingly entrenched inflation pressures, make this a high risk stock market. The Federal Reserve is heading toward a monetary showdown, and inflation news isn’t getting any better

In recent months, we laid out warning flags to watch — from the speculative frenzy to the mega-cap momentum stocks to internal leadership and all-important investor psychology.

The good news is we’ve been preemptively defensive in our portfolio decisions. The bad news is those warning flags are starting to sequentially drop into place and resemble some of the most significant bull market tops in history.

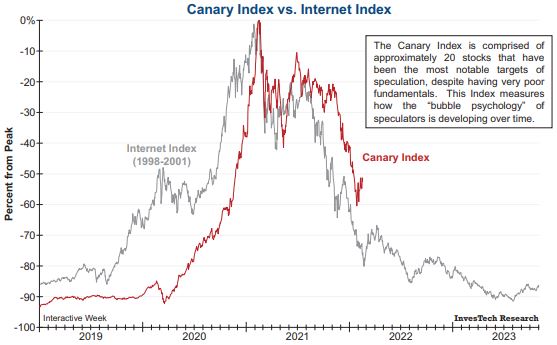

Major bear markets typically unwind in stages, with the areas of greatest excess falling first and often precipitously. Nothing has been more emblematic of this dynamic than the downfall of the Interactive Week Internet Index during the popping of the Tech Bubble in 2000.

After the peak in the S&P 500 on March 24, 2000, the highly speculative Internet Index fell by -36% in six weeks — a strong signal that the speculative mania was starting to unwind.

In recent years, ultra-accommodative monetary policies from the Federal Reserve have led to a similar speculative frenzy. Our Canary (in the coal mine) Index is representative of the current speculative excesses, as it contains approximately 20 of the most overhyped, overbought, and overvalued stocks in the market over the past two years.

The graph below shows the surprising comparison between the Internet Index of the late 1990s and our Canary Index today. While the Canary Index has already lost more than half its value from the February 2021 high, the fact that the Internet Index ultimately lost over -90% suggests that the Canary Index stocks likely have further to fall.

After the areas of greatest excess have started to unwind, the next bear market warning flag to watch for is a breakdown in the mega-cap momentum darlings of Wall Street.

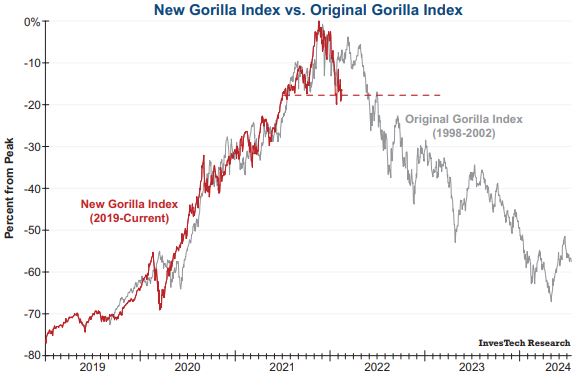

Stepping back to the Tech Bubble, we created our original Gorilla Index in 1998 when it became evident that a relatively small group of mega-cap momentum stocks were responsible for the majority of the market’s advance. This Gorilla Index contained only 17 stocks, yet it accounted for a quarter of the S&P 500’s market capitalization at the time.

While the Gorilla Index held up relatively well for the first six months of the 2000-2002 bear market, it ultimately broke down, sending a message that major institutions were scrambling to raise liquidity and reduce market exposure.

Following the market rebound out of the COVID-19 Crash, we created the new InvesTech Gorilla Index, as an extremely narrow basket of mega-cap momentum stocks had once again become a dominant portion of the S&P 500. Today’s Gorilla Index contains only ten stocks, yet it accounts for an even greater share of the S&P 500 (27%) than the original version.

The graph below shows the new Gorilla Index as compared to the original from 1998 to 2002. While we know that the underlying dynamics during both periods share similarities, it is truly staggering to see how closely their trajectories have aligned up to this point.

The new Gorilla Index has been a bit quicker to unwind thus far (with a maximum drawdown of -20% from its peak) and is now near a critical support level. If today’s Gorilla Index definitively breaks down, the S&P 500 will undoubtedly follow, and additional losses will lie ahead for this basket of mega-cap momentum stocks if we are indeed in a bear market.

Evidence is clearly warning that an important top is likely in place; yet the jury is still out on whether this will be a protracted correction or a major bear market. However, we know that every bear market started out as a correction, and every big bear market started out as a small bear market. And that makes the next 60-90 days perhaps the most critical in this market cycle stretching back to its start in 2009 (COVID-19 Crash excluded).

As market historians, we know that all market cycles are different. But, when it comes to the messages being sent by our Canary and Gorilla Indexes, the similarities to the unwinding of the Tech Bubble are striking.

Major bear markets like the Tech Bubble tend to unwind in stages marked by a sequential loss of confidence, rather than “popping,” as is so popularly assumed. Preemptively avoiding the most speculative and overvalued areas of the market paid off handsomely as the NASDAQ and Gorilla Index fell harder and faster than the broad market (S&P 500).

There is no crystal ball when it comes to navigating the eventual end of a market cycle. Rather, a disciplined assessment of the weight of the evidence allows you to proactively position your portfolio to be defensive when it really matters. Going forward, we are prepared to further increase portfolio defenses depending on how the indicators unfold,

In the end, navigating a (probable) bear market is not about putting your money under a mattress and waiting for the sky to fall. Instead, the focus should be on proactively managing risk to carefully navigate a wide range of outcomes and positioning oneself for that next great buying opportunity.