On days when the stock, bond, and commodity markets decline but the dollar goes up, the only clear conclusion is cash is being raised and stuffed into money market funds. That pattern of behavior is putting downward pressure on the very short-end of the curve while the long-end is still trending higher, explains Eoin Treacy, editor of Fuller Treacy Money.

The net result is the 10-year – 3-month yield curve spread is now recovering from deeply inverted territory. Meanwhile, the belief in a soft landing is predicated on rates coming down soon and liquidity remaining supportive indefinitely. The more people believe and act as if that is reality, the less likely a soft landing is.

The next inflation figures will be released on Friday and the one to watch will be Core Services Less Housing. It has been stubbornly high, and I don’t see any particular reason it will decline significantly on this reading. That will only further support the argument for keeping rates higher for longer.

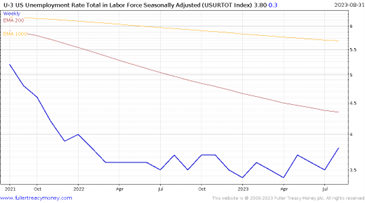

Meanwhile unemployment has made a new recovery high. It is still below 4% but the trend is now moving higher. Rising unemployment and high inflation is a nasty stagflationary recipe, which is unlikely to be beneficial for stock prices.

The Nasdaq-100 also just made a new reaction low as it continues to unwind the short-term overextension relative to the 200-day MA. I believe the most likely scenario is a deeper process of consolidation as the ability of consumers to sustain their pandemic lifestyles comes under additional pressure.