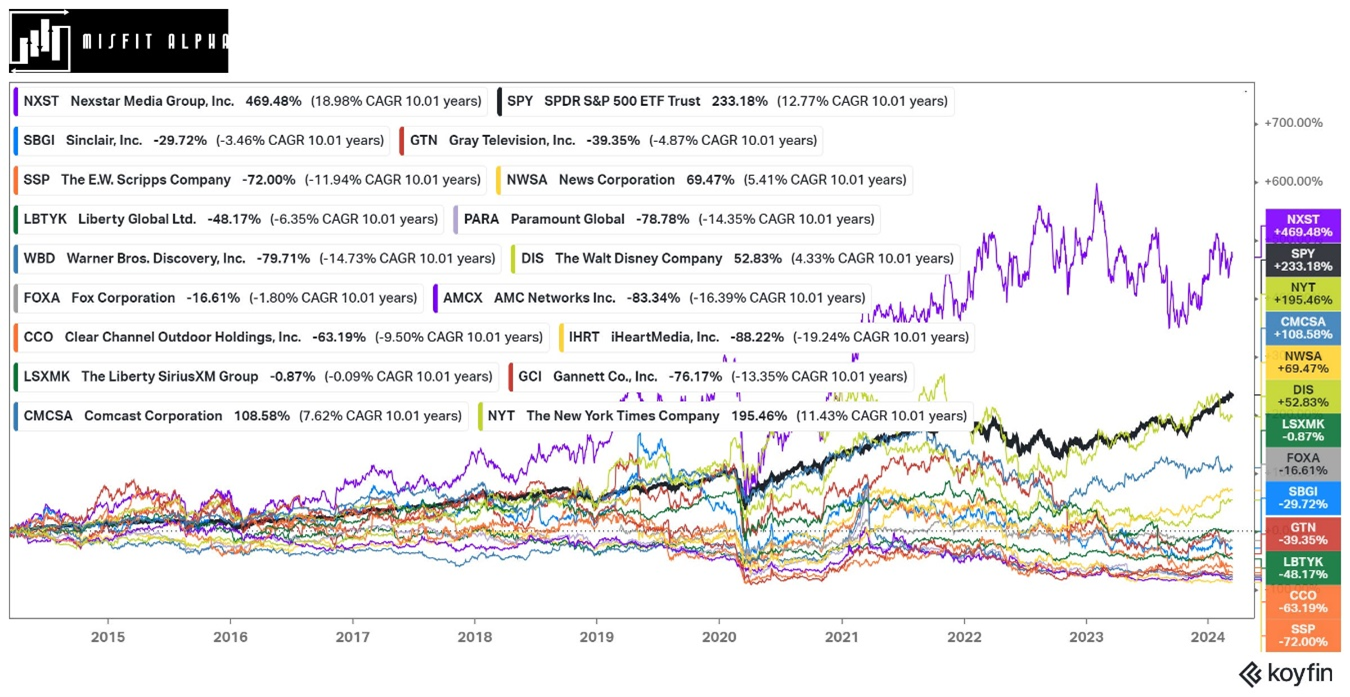

The media industry has, arguably, the worst ratio of industry returns to how much the industry is discussed or analyzed. Over the past couple of decades, media is where investors’ capital has gone to die. So when I started sorting through the list of companies that have beaten the market over the longer term (at least 15 years), I was surprised to find one media company on the list: Nexstar Media Group Inc. (NXST), explains Tyler Crowe, author of Misfit Alpha.

Since Nexstar’s IPO in late 2003, it is the only non-Netflix (NFLX) media company to beat the S&P 500 on a total return basis.

I’m as surprised as you to find an “old” media company on the list of long-term, market-beating companies. This glaring outlier in the industry leads to a big question. How has this one company succeeded in generating shareholder returns when so many others have failed? Is Nexstar really better at running a non-Netflix media business than anyone else in the US?

Nexstar is not a household name, but it is the nation’s largest local television broadcasting group, with over 200 owned or partner stations in 40 states and Washington. It owns 75% of The CW, now America’s fifth-largest broadcast network (behind ABC, NBC, CBS, and FOX). It also owns cable news channel NewsNation, multicast networks Antenna TV and REWIND TV, and a 31.3% stake in TV Food Network..

Nexstar has deliberately positioned itself to benefit from political advertising. It has broadcast stations in 80% of the markets that had a contested political election in 2022. It has assets outside of television, but the revenue from its website portfolio is fractions of its television money, so it’s hard to justify making its digital products a core part of anyone’s investment thesis.

Its positioning in swing-state and contested election markets means it can better hoover up political campaign advertising budgets. Also, by electing not to develop an in-house streaming platform, it has avoided the costly and low-return spending that has plagued other programming networks like Paramount Global (PARA) and Warner Bros. Discovery Inc. (WBD).

Over the past decade, a significant industry roll-up strategy has been another separating factor between its peers and the most likely source of its outperformance. When it went public in 2003, Nexstar was a small fish in this business. At the time, revenues were only $214 million. By the end of 2011, its revenue had only grown to $306 million and it remained largely unprofitable. Starting in 2012, though, it underwent a strategic review and went on a buying binge.

But while the company has received a BB+ credit rating, it took on much of its debt from acquisitions in a much lower interest-rate environment. I’m not going to say that Nexstar’s rise was a ZIRP phenomenon only, but was there ever a better decade to go on a debt-fueled acquisition spree?

While broadcast stations and linear television will likely remain a business for a long time, that doesn’t necessarily mean it will be lucrative. Nexstar has been an industry outlier for the past twenty years, but it does not have anything resembling a durable and lucrative moat for the next twenty.