Investors are on edge as 2019 approaches. Given the age of the current bull market, investors are anticipating the end. With the memory of 2008/2009 still fresh and resurfacing of volatility in 2018, investor anxiety is reaching new highs, writes Lindsey Bell Thursday.

Throughout 2018, the S&P 500 (SPX) entered into correction (a decline of 10% - 19.9%) territory twice, with the most recent correction occurring Thanksgiving week. As we look forward to 2019, CFRA digs into the top six risks facing the market, starting with what we view as the least concerning and ending with our biggest concern.

We focus on domestic issues here, leaving global risks for another time. We rank them starting with 6, down to 1.

6. Inflation – This was the year that inflation was expected to skyrocket, driven first by fiscal stimulus and then further boosted by tariffs (more on that below). The Fed’s favored inflation metric, core PCE, which excludes food and energy, crossed 2% in July for the first (and only) time since 2012, but has hovered under that level for most of the year.

October’s increase of 1.8%, puts inflation slightly below the Fed’s target rate of 2%. Rising costs of raw materials, transportation and labor are beginning to put pressure on corporations and that could translate into higher rates of inflation, but offsets will likely be driven by advancements of technology and the Amazon (AMZN) stranglehold on the price of many final goods.

The forward breakeven rate of inflation, which is based on fixed income investors’ expectations of inflation over the next five years, stood at 2.04% on Tuesday (Nov. 27). That rate has crossed 2.25% a couple times this year but has consistently declined after crossing that threshold each time. Action Economics expects core PCE inflation to reach 2.1% at the end of 2019.

5. Peaking EPS – First-quarter EPS growth of 23.3% was feared to be as good as it gets for quarterly earnings growth from the S&P 500 in this cycle, thanks in part to a comment from the Caterpillar (CAT) CFO in April. That proved to not be the case with second-quarter EPS growth of 25.2% topping first-quarter and then third-quarter EPS growth of 28.5% even better than second-quarter.

The run may come to an end with fourth quarter as the current consensus estimate is 15.3%.

What’s for sure is growth in 2019 will slow substantially; consensus estimates point to 7.5%, down from the 22.9% expected in 2018.

Outsized growth will be tougher to come by as the tax reform benefit and other fiscal stimulus is lapped. Slower growth typically comes with lower price-to-earnings (P/E) multiples. Year-to-date, the forward P/E has averaged 17.1x. In 2014, the last year to show EPS growth of about 7.5%, the forward P/E averaged 15.9x, which is in line with the current forward multiple of the S&P 500.

In 2012 and 2013, EPS growth averaged 5.3% and the average forward P/E multiple over those two years was 15.1x. Thus, the market multiple may decline a bit more, as growth slows and interest rates rise.

4. Rising Interest Rates/Monetary Policy – The fear that the Fed, with a new chairman at the helm, will raise interest rates faster than the economy can handle has resulted in many sleepless nights for investors. After raising rates once each in 2015 and 2016, the Fed has raised rates three times this year with expectations for one more increase at the December 18-19 meeting at 82.7% according to the CME Group, a marketplace for options and derivative contracts.

While members of the Fed are split between whether to raise rates two, three or four times next year, the probability of three rate hikes next year has been declining.

Fed Chair Jerome Powell eased investors' concerns Wednesday in a speech where he described interest rates “just below” the neutral rate. This implied that the number of interest rate hikes left will be minimal. Read the full Powell transcript here.

It is likely that escalating weakness in housing has caught the Fed’s eye. A reduction in consumer confidence and a slowdown in business investing may also be playing a role. Most importantly, inflation is holding steady under 2%, which reduces pressure to raise rates quickly.

Further, according to Sam Stovall, CFRA Chief Investment Strategist, history reminds us that no bear market in more than 60 years ever started with the difference between Fed funds and headline CPI inflation this narrow (currently at -0.38). Indeed, just before all bear markets since 1955, the Fed Funds rate was higher than the y/y change in headline CPI by an average of 2.5 percentage points.

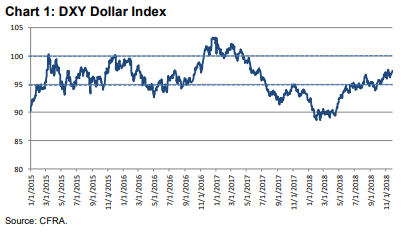

3. Dollar Strength – Much time has been spent talking about the strength of the U.S. dollar (USD) in 2018. Would you believe me if I told you the dollar was down 3.8% on average year-over-year for the year-to-date period through Tuesday? In fact, the quarterly dollar average, using the Dollar Index, (DXY) which measures the value of the dollar to a number of other currencies around the world) has declined year-over-year in each quarter of the year.

The dollar is important because 43.6% of S&P 500 revenue is derived from outside the U.S., according to S&P Dow Jones Indices. Looking at a longer-term chart of the dollar, it is now more in line with 2015-2016 levels. The currency lost steam in 2017 as synchronized global growth gained momentum.

The rebound started in April 2018, as trade tensions rose, political uncertainty abroad increased, interest rates moved higher and the global growth story slowed. Action Economics expects the dollar to increase 3.9% in 2019. That would weigh on the market as pressure is applied to top-line growth, but would bring the dollar back to 2017 levels, reversing the decline of 2018.

2. Corporate Debt – Corporations have been loading up on debt with low interest rates to fund stock buybacks as the S&P 500 reached new highs over the last several years. Corporate bonds outstanding at the end of Q2 totaled more than $9.0 trillion and the corporate debt to GDP ratio exceeded 45%, marking a new cyclical high.

During the last three cycles, 45% was the ceiling for this ratio, indicating corporations had reached debt capacity. There are reasons this time could be “different” and such a high ratio is sustainable near-term, including the more global nature of businesses as well as the unusually low interest rates.

Despite the amount of debt rising, the default rate has declined, a trend that is contrary to historic trends. In addition, the issuance of BBB, or the lowest level of investment grade (high quality) debt dwarfs A-rated bonds, according to Chris Kuiper, CFRA Senior Equity Analyst. Moody’s puts this into perspective by stating that the dollar amount of outstanding U.S. investment-grade corporate bonds “is now riskier than it was prior to each recession since 1981 and possibly all prior downturns through the late 1940s.”

1. Trade/Tariffs – Trade has been a wild card throughout 2018. The level of uncertainty derived from the U.S./China trade relationship has intensified as the year progressed. President Trump has threatened to raise tariffs on $200 billion worth of goods imported from China to 25% in January, from 10% currently. He may also tariff the remaining $267 billion in imports from China that are not currently taxed (at a rate of either 10% or 25%). Trump and Chinese President Xi Jinping are set to meet at the G-20 meeting in Buenos Aires over the weekend. There is much speculation if the two sides will come to an agreement for a ceasefire on tariffs or a plan to resolve their trade differences.

Given mixed signals from various members of the Trump administration, Wall Street is unsure what to expect from the meeting of the leaders of the two largest economies in the world. Estimates for how these tariffs will impact the economy vary.

The Tax Foundation estimates that the impact of all enacted and announced tariffs, including those on / from other countries besides China and the U.S., would be a 0.59 percentage point decline in U.S. GDP in the long-run. For context, Action Economics currently expects 3.0% GDP growth in 2019. The long-term impact doesn’t sound terrible, but the Tax Foundation’s estimate doesn’t include what tariffs might do to business sentiment and how that will change investing and hiring decisions.

The uncertainty from trade could compound the situation with the downside increasing the longer the dispute goes on. Additionally, the uncertainty will bleed into the global economy, potentially leading to a broader global slowdown and making many of the previous listed concerns much bigger problems.

Please consider registering for an S&P Global webinar I will be participating in titled “Emerging from Home Bias with Passive Strategies” on December 6 at 2 pm. Information here.

View CFRA, services and research including Marketscope Advisor here.

View brief video interviews with Lindsey Bell of CFRA:

Lindsey Bell’s picks: Apple, AI, Nvidia, Intel, semiconductors here.

Duration: 3:14

Q2, Q3, the worst. Q4 good news here.

Duration: 3:53

Recorded: MoneyShow Las Vegas, May 15, 2018.