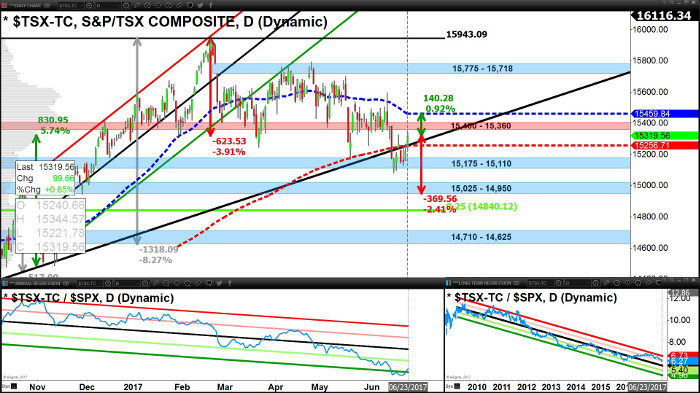

Recent break of the 200-Day Average (15,257) leaves the market open for a dead-cat bounce, which started last week. Our TSX market is more reactionary to Global-Macro catalysts, asserts Ziad Jasani of the Independent Investor Institute in his weekly Trader video.

Here is my outlook for the TSX and global equities for the remainder of this week, and the following weeks and months.

Short-term outlook this week

With Oil readying for a bounce, and Energy Equities confirming swing-low-formations into the end of last week (June 23), we see a dead-cat-bounce on the TSX taking it back to resistance of 15,400-360 but leaving it below resistance of its 50-Day Average (15,460) this week.

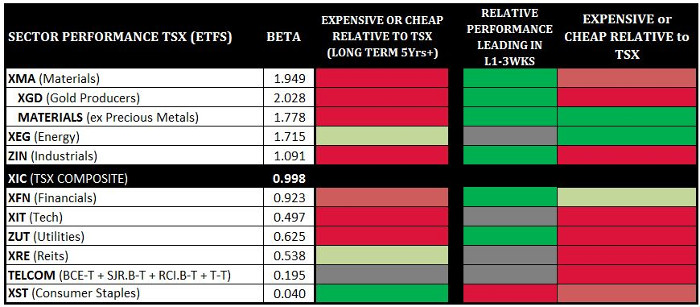

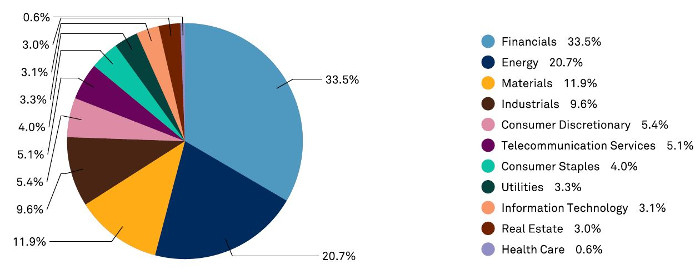

We see short-term merit in long Energy, Materials (except Gold), and Financials within Canada this week. Sectors more likely to out-perform this week are:

Financials iShares S&P/TSX Capped Financials Index Fund (XFN)

Energy iShares S&P/TSX Capped Energy Index Fund (XEG)

and Material Stocks except Precious Metals.

While under-performance would be expected from:

Telecom

Staples iShares S&P/TSX Capped Consumer Staples (XST)

Utilities BMO Equal Weight Utilities Index ETF (ZUT)

Tech iShares S&P/TSX Capped Information Technology Index ETF (XIT)

and REITs iShares S&P/TSX Capped REIT Index ETF (XRE),

Industrials BMO S&P/TSX Equal Weight Industrials Index ETF (ZIN)

and Gold Producers IShares S&P/TSX Global Gold Index ETF (XGD).

TSX trading levels & short-to-mid-term strategy

Tariffs, Mortgage Market Risk, Oil weakness since early April, and Trumpflation NOT reigniting are all keeping the TSX in a sideways range with a down-tilt.

Recent break of the 200-Day Average (15,257) leaves the market open for a dead-cat bounce, which started last week.

Remember, our TSX market is more reactionary to Global-Macro catalysts, currently sentiment towards global growth is fragile and key to holding prices up at these market highs.

The TSX has arguably fully priced-in Trump’s plans wherein any negative shifts in sentiment towards these plans pose greater downside risk for the TSX.

Note: The TSX has broken an up-trend channel from November 2016, and had been under-performing the world (ACWI) and the S&P 500 since 2017 started, with a small round of out-performance March 20th – late April.

Out-performance was led by the defensive sectors: REITs, Utilities, Staples, Telecom.

Defensives are now dislocated and expensive while cyclicals are cheaper on annual routines; suggesting a top or if Trumpflation resumes, a pop. The break and close below 15,400-360 and the 200-Day Average (L2Wks) was a sell-signal for the swing-portion of mid-to-longer-term holdings and signaled closure of any long-side trades in the short-term.

However, the TSX is in a bounce that likely takes it back to resistance of 15,400-360 this week, which can be played using shorter-term capital 3 areas: Financials, Energy, Material stocks.

Mid-to-longer-term outlook (weeks-to-3 months+)

The TSX is dislocated and expensive on long-term routines with the S&P 500, but has neutralized vs. the world iShares MSCI ACWI Index ETF (ACWI). This implies under-performance is more likely over the next month vs. the S&P 500 (sideways to down-trending action).

The most vulnerable spaces in our market are Gold Producers, Technology, Utilities, REITs, Telecom, Staples, Industrials and Material Stocks (not precious metals related): XGD, XIT, ZUT, XRE, XST, ZIN, Bell Canada Enterprises (BCE).

Our Energy sector is relatively cheaper on annual routines and suitable for short-term bounce plays but not longer-term investing; as Energy (XEG) peaked in December 2016 and Oil is likely stuck in a long-term sideways range.

Financials (XFN) are on the cheaper side of Annual routines after underperforming since late February 2017 (Trumphoria dissipating) making bounces on positive headlines viable.

However, a break and close below support at $34.80 would be another sell-signal.

View the latest videos from Ziad Jasani of the Independent Investor Institute here