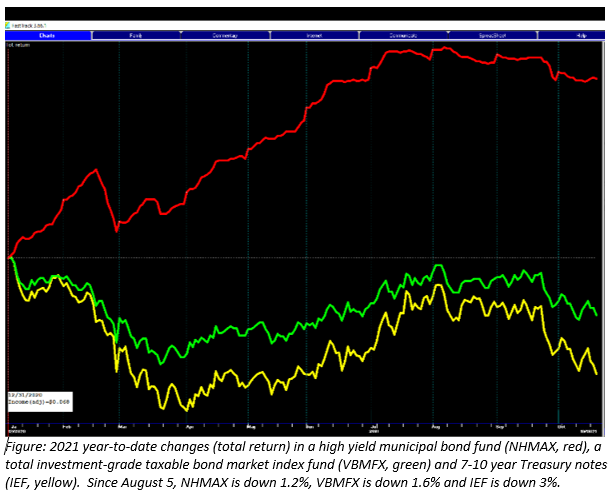

As long-term interest rates have risen since the start of August from 1.17% to 1.63%, both investment-grade bonds and high-yield municipal bonds have sold off, explains Marvin Appel of Signalert Asset Management.

In the case of high-yield municipal bond funds, declines from August – October have ranged from 1.2%-1.8%. In comparison, the Vanguard Total Bond Market Index Fund (VBMFX), a taxable investment-grade bond fund) lost 1.6% over the same period.

Considering that high-yield municipal bond fund portfolios have longer maturities (typically nine years’ duration) than the average investment-grade bond (6.5 years), high-yield municipal bond funds have held up better than one might have feared. Year-to-date, they remain one of the best areas of the bond market. The benchmark S&P High-Yield Municipal Bond Index is up 5% in 2021, compared to much smaller gains in investment-grade munis (S&P Municipal Bond Index up 0.9%) and to a total return loss of 2% in investment-grade bonds.

Nonetheless, the question remains whether it is a good time to take profits in high-yield municipal bond funds or to ride out the declines of the past eleven weeks in anticipation of a recovery. My assessment, as described in more detail below, is that the sell-off in bonds is near its end. This may be a good time to add capital to a high-yield municipal bond strategy.

Treasury Yields and Inflation Expectations Are Retesting Their March-May Highs.

Except during idiosychratic periods where there is a liquidity crunch surrounding bearish sentiment in municipal bonds, high-yield municipal bond funds tend to track price changes in investment-grade bonds. That means that the outlook for high-yield municipal bonds is similar to the outlook for intermediate or long-term Treasuries after their sell-off.

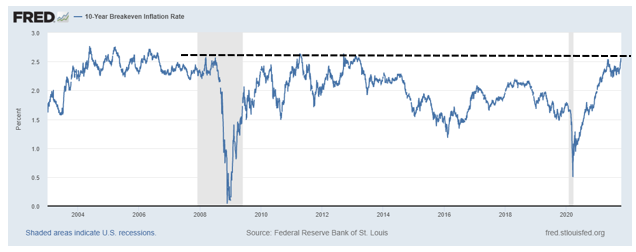

The chart below shows the level of inflation that treasury note prices project for the next 10 years. This is the inflation that will make the total return of 10-year treasury inflation-protected securities the same as the return from 10-year Treasury notes from now through maturity. Now at 2.54% per year, inflation expecations are at their highest since 2006 (dashed black line). Even if projected inflation makes a new 15-year high, the previous peak from 2004-2006 was in the 2.7% range, not far from current levels (2.54%).

While it is always possible that inflation expectations will make highs not seen since the 1990s, betting on multi-decade highs is inherently a long shot. As a result, I expect 10-year inflation expectations to hit a peak not far above current levels, which would also place a ceiling on one of the two main forces driving interest rates higher. (The other factor is the Fed starting soon to taper its bond purchases, which should already be factored into bond prices.)

What about interest rates themselves? 10-year Treasury note yields have been much higher, hitting 3.2% as recently as 2018. However, yields collapsed once they got that high as the economy sputtered. Back in 2018, when the economy couldn’t tolerate a 10-year yield of 3.2%, debt / GDP was at 340%. In the wake of the pandemic, that ratio spiked to 415%. With the economic recovery since mid-2020, the debt / GDP ratio in the US has pulled back to 376%.

This represents a debt burden of 10% more than back in 2018, when a 10-year Treasury yield of 3.2% was intolerable to the economy. If a smoothly running economy couldn’t tolerate 3.2% rates three years ago, our current economy burdened by more debt and rendered more fragile as the result of labor shortages is all the more unlikely to support yields that high. History suggests that over the very long-term, an economy like ours, with a projected real growth rate of 1% and inflation in the 2% range, should sustainably support 3% yields on 10-year Treasuries. But it will take us years of reining in debt growth to get to the point where the economy can remold itself to accommodate historically more normal interest rates without plunging into recession.

Looking at the circled area in the chart of 10-year Treasury note yields below, we should be in an area of resistance including the 3/31/2021 peak of 1.75% or the November-December peak of 1.95% in 10-year yields.

Implications

We maintain two high-yield municipal bond fund timing models for client accounts, and they are delivering a split verdict: one on a sell and one on a buy. (The newsletter position in NHMAX has a wider stop and remains on a buy by a significant margin.) It appears to me that investment-grade bonds are oversold in the intermediate term (weeks-months). However, with yields and inflation expectations now near levels where they have historically stalled, additional price declines in bonds are likely to be contained. As a result, if you are looking to add to positions in high-yield municipal bond funds, this should be a good time.

One way you can hedge your bets is to buy the Nuveen Short-Duration High-Yield Municipal bond fund (NVHIX). You will be giving up about 1/3 of the yield (approx. 90 bp) compared to the Nuveen High-Yield Municipal Bond Fund (NHMAX), but you will be exposed to less than half the interest rate risk (duration of 4.3 years for NVHIX vs 10.2 years for NHMAX).

To learn more about Marvin Appel, please visit Signalert Asset Management.