One of my favorite rotations to time is from value to growth, and vice versa, states Samantha LaDuc, of LaDuc Trading.

As a macro-to-micro analyst, educator, and trader, I work to find durable trends to trade with and around for my clients. One such trend has been that of higher inflation, yields, and value/cyclical trades since summer of 2020, using tech as a bond proxy for lower rates.

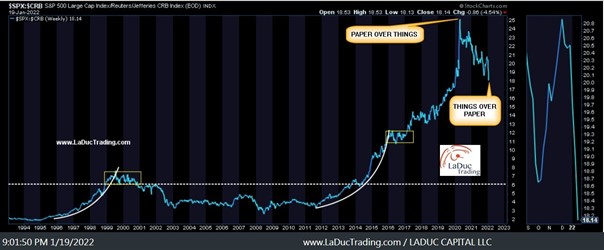

This is not a new view for me. I have been an “inflationista” and rates bull/bond bear since July/August of 2020. My mantra of things over paper and inflation is sticky have been repeated often enough so that clients know I still hold that view as we enter the new year of 2022.

Two related core themes from early 2021 will carry into my 2022 trading and investing plan and revolve around my thesis that: “Deflation ended with covid” and “Oil as an inflation hedge“. These macro-to-micro themes have been detailed in client posts since March 2021 with the macro, intermarket, and technical backdrop to support my view. Suffice it to say, these themes have proven to be both durable and profitable, and together they set up my top 2022 prediction—that of a sizable growth to value rotation in stocks. Here is a brief overview of my main reasons why:

- Stagflation: As supply stress has shown, demand for things has outstripped supply of things, which is another way of saying too much money is chasing too few goods. Investment in meeting pent-up demand likely drives a CAPEX revival which drives the value/cyclical plays. Big picture, the case for things over paper—hard assets over paper tech returns that were built on excess speculation from excess Fed liquidity—is reversing with a quantitative tightening and higher rate regime, not to mention global manufacturing breakdown and labor shortage.

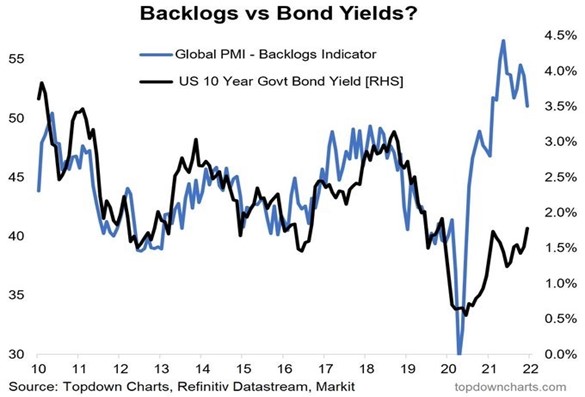

- Backlogs: Supply bottlenecks and shipping/manufacturing breakdowns have driven in large part inflation expectations. Backlogs have not caught up. Yields overlayed with backlogs point to bond-yields rising for some time. This is a pressing risk to bond proxies, such as tech.

- Inflation Expectations: The reason for the season behind Fed’s recent hawkish pivot is because of clearly persistent and sticky inflation giving rise to inflation expectations. From China exporting inflation back to us in the form of shipping and manufacturing shortages and delays to higher US energy, housing, car, food, and wage costs. Inflation is driving Fed action to raise rates and run-off its balance sheet sooner rather than later. Higher yields pull commodities higher, which benefits sectors with concentration in real-world goods, especially large cap value.

- Monetary: With a 7% inflation rate (highest since 1982) and a 4.2% unemployment rate (vs. 5.8% historical average), the Fed has held interest rates at 0% and added over $1.3 trillion in assets to its balance sheet in 2021. Inflation (they have finally admitted) is not transitory, but (I contend) it is political. Fed’s reversal to a hawkish rate regime—in front of mid-term elections—has driven expectations for an accelerated pace toward higher rates. My view: Fed is incentivized to speed up its debt roll-off through reduced bond purchases (tapering) to get to the part where it starts raising rates (QT)—all in order to tap down inflation (for political expediency).

- Real Yields: The real Fed Funds Rate of -6.7% we achieved in 2021 is the lowest we’ve seen since 1974. As real yields normalize (rise) back toward zero, more traditional factors, like value, start to gain traction.

- Valuations: Thirteen years of Nasdaq out-performance is an outlier, thanks to easy monetary conditions and copious amounts of QE liquidity. With Fed now shifting to tightening, market is transitioning from high P/E ratio stocks to low P/E value/cyclical plays. More to the point, growth stocks—small and large cap—are trading at a premium despite a recent pullback. Value is still very undervalued.

- Active vs Passive: Passive investing has had the tailwind of Fed backstops for fourteen years. Buy and hold works great in bull markets and bubble markets, but not in bear markets. Another observation: SPX has outperformed thirteen years in the same way gold returned ~18% per annum from 2000 to 2011, before gold topped and moved sideways in large part over the past decade. It would not surprise me for growth to under-perform this year and into the next few years.

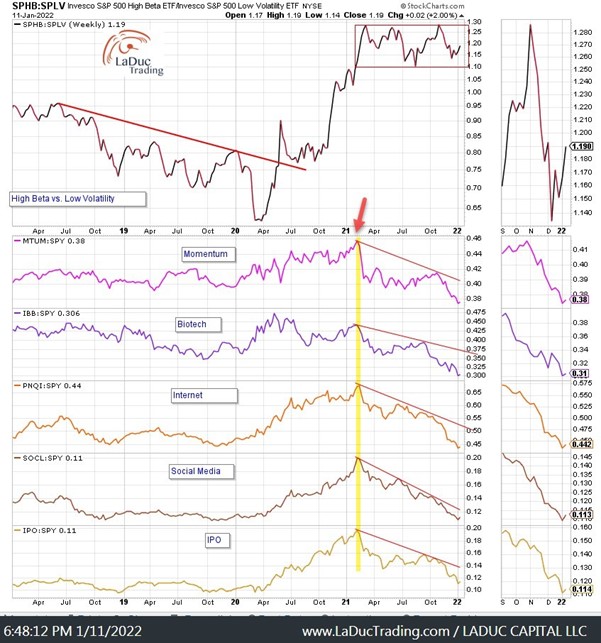

- Divergences: Low Volatility vs High Beta has outperformed during much of November and December, and into January. The rotation out of “unprofitable growth tech” (MTUM, KWEB, SOCL, IBB, PNQI, SOCL, IPO) peaked back in February of 2021 relative to SPY and is unlikely, in my opinion, to reach 52 week highs any time soon. What has held markets in place was the FANGMAN+T contingency, but in fact despite higher indices heavily weighted in mega cap tech, the proxy $NYFANG returned a flat total return for 2021. This is the definition of a “Market in Distribution”.

- Tech Wreck: The soldiers of small and mid-cap “explosive, unprofitable growth” plays—from ARKK to SPAKs constituents and many other speculative tech plays in between—have corrected under the surface of Nasdaq top-line price action to realized drawdowns from 20 to 80% from their highs. It is only natural for the generals of mega-cap tech FANGMAN+T to be tested. Most are expecting midcap tech to be bought and rebound back to 52 week highs in 2022. I suggest this group of mega cap tech will be challenged in a rising rate environment that serves as headwind with supply chain stress, labor shortages, and margin contraction (read: earnings disappointments).

- Sentiment: After a turbulent period past two years with our global health scares, I suspect we learn to live with Covid (and all its variants), and that government restrictions lighten. Yes, it’s an early narrative, but I believe people now want to get back to work, school, and leisure routines as the efficacy of vaccines gets debated and panic abates. This normalization helps support economic productivity, consumer sentiment, and spending…driving real-world (and much needed) economic stabilization and organic growth. This is conducive to the cyclical/value stock rotation, even as a stronger economic backdrop emboldens the Fed to tighten.

- Fiscal: Political action to pass sweeping legislation into mid-terms will be challenging, but current administration has promises (and seats) to keep. At the same time, this promised addition of fiscal liquidity helps replace in part the removal of Fed liquidity. With an economic growth backdrop of 4% expected for 2022, fiscal stimulus in the form of more infrastructure and investment in communities (people and projects)—versus monetary easing that benefits banks and big businesses—is a tailwind for reflation stocks.

- Volatility: As creatures of habit, we are probably better at predicting what won’t change than what will. But one thing I predict that will change is volatility. The worst drawdown for SPX barely scratched 5% in 2021. That’s a very low bar to beat for 2022! This is another reason I believe low volatility stocks will very likely out-perform high beta as volatility emerges to reprice the riskiest of assets.

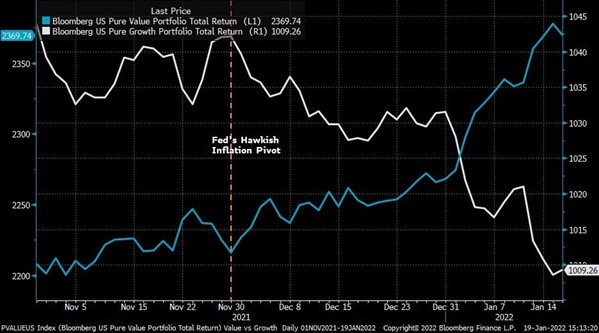

- Intermarket: My growth-to-value analysis triggered November 29, signifying that the rotation from growth to value has begun. Curiously, this timed with when Fed retired “transitory” in its speaking points about inflation. The divergence between value and growth has accelerated into 2022, with pure value factor up 4.5% YTD while pure growth is down 2.2%. I think this is just the beginning.

Summary:

The synchronization of buying every dip the past two years has been stunning. I contend, at some point this year, the buyers will step away and let gravity take hold. Given that about one-third of investors are new, and margin buying has seemed to peak and start to roll over, I would contend that 2022 will set the stage for problems that will test our new traders and our old 40-year long macro frameworks. The Fed Put has moved, and since 2013 taper tantrum, I would wager it sits about 20% below current market prices.

Basically an accommodative Fed reduces volatility. A tightening Fed, by definition, triggers it. With that, value should lose less than growth at the very least, if not straight-out outperform.

Learn more about Samantha DeLuc by visiting LaDucTrading.com