Last year I felt like the Paul Revere of investing, letting everyone know that higher rates were coming, notes Steve Reitmeister of Reitmeister Total Return.

At first, I looked quite foolish as rates stayed near historic lows even as the Fed clearly signaled their higher rate intentions. But saying and doing are two different things when the Fed dominates the bond market with their obscenely large $9 trillion balance sheet.

So as the Fed actually got to the doing part...and there were more bonds freely floating on the open market, that indeed got rates rising in a hurry and now approaching an interesting juncture at 3% for ten-year Treasuries.

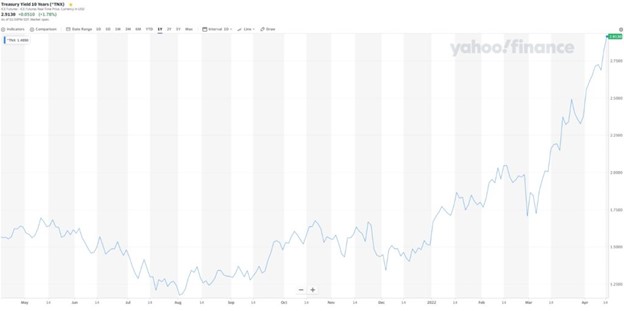

Let's talk about the journey that got us here...what happens next...and what that likely means for the stock market. Let’s start with a chart of the 10-Year Treasury Note Interest Rates (TNX) over the past twelve months.

Truly this is the tale of two very different time periods. The first half with the Fed talking up their desire to raise rates with no real movement taking place.

The second half is a more than doubling of the rate from 1.34% in early December 2021 to just shy of 3% today.

This is great news for Reitmeister Total Return members as we have seen our largest position, ProShares UltraShort 20+ Year Treasury (TBT), rally +54.81% in that short time frame.

However, this was bad news for many other investors as they have relied upon low rates as a seemingly permanent floor, supporting higher and higher stock prices. And yes, I also beat that drum pretty loudly under the banner of this being a “TINA” stock market.

There

Is

No

Alternative…to owning stocks

The theory is that when rates are this low, “cash is trash,” as you will not make enough interest on your savings to cover the rate of inflation (that is shockingly true now).

Secondly, the rising rate environment is also a death knell for bond investments as rising rates = bond value losses. That is a wake-up call to folks who incorrectly thought that bonds were a safe haven after a nearly 40-year bull market in bonds.

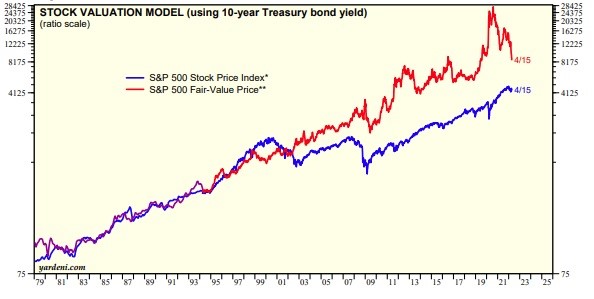

Add these together and it says that stocks are the best value in town. And honestly, that is still true today, as can be seen by the following chart:

This is an interesting comparison of the Earnings Yield of stocks versus the yield on ten-year Treasuries. What the left side of this chart shows is the historical norm. That being a world where the value of these two popular investments was basically in parity.

However, as the Great Recession came around, Fed Chair Bernanke unveiled his low rate playbook which got the economy and stock market back on track. That’s because, in a low rate environment, everything looks better than cash and bonds, leading to more risk-taking (like investing in businesses) which spikes the economy and stock market.

That playbook took on new meaning during the Covid crisis when the stock market bounced in late March even while the economy was being flushed down the toilet. Here again, because everything looked better than cash or bonds when rates reached these new historic lows.

Back to the point…even with rates on the rise back to almost 3% in the present day, this chart proves that stocks are still the best investment in town. Because it says that parity value with the bond market would equate to a near doubling of the stock market from current levels.

This is the key reason why you need to keep a bullish bias in place even as inflation rages on…the Fed is getting more hawkish…and Russia keeps up its attacks on Ukraine. Because as we look at our investment options, we find that we are still very much in a "TINA" environment that points to higher share prices on the way.