Internally, we were talking yesterday about the energy space and the recent pullback in prices, states Sean McLaughlin of AllStarCharts.com.

While still the strongest sector in the market in 2022, this move off the highs has been notable.

Is the trend over? Or was that just the “hot money” taking profits?

I’m not sure we have a definitive answer to that question yet. It looks to me that the market is still sorting that out. And this condition of indecision, coupled with high implied volatility priced into options is combining into a nice opportunity to collect some options premium while energy figures itself out.

So we’re going to wade into the energy pool with a delta-neutral short-premium options trade.

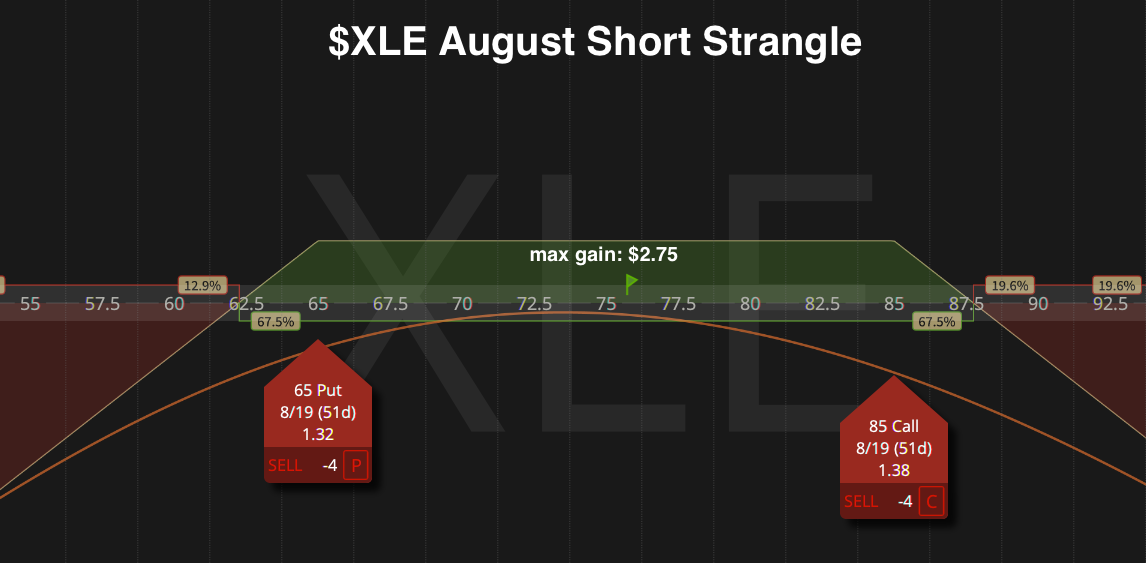

As you can see in this chart of the SPDR Energy Fund (XLE), the 65 level on the downside has some price memory and 85 on the upside feels comfortably far enough away to give us plenty of wiggle room:

Additionally, these levels are notable to me as each of those strikes is currently priced beyond a one standard deviation move at current XLE prices.

We’re going to put ourselves into a position with a high probability (though certainly not a guarantee) of profit.

Here’s the Play

I like selling an $XLE August 65/85 Short Strangle for an approximately $2.75 credit. This means we’ll be naked short equal amounts of the 65 puts and 85 calls:

This position will require margin due to the unlimited risk inherent in naked options (if naked risk makes us uncomfortable, we could “buy the wings”, purchasing the 60 puts and 90 calls to convert this position into a defined-risk Iron Condor position).

As such, we’ll be vigilant in managing risk in this position.

Our thesis is that XLE will stay within the range of 65 to 85 over the next several weeks. As long as that remains true, we will have no trouble getting out of this position at a profit. We’ll leave a resting GTC (good-till-canceled) order to buy this spread back for a $1.35 debit. This will capture 50% of the original premium collected without the risk of having to hold this position all the way until August expiration.

In the meantime, if XLE sees a daily closing price below 65 or above 85 (outside of our short options strikes), then this proves our rangebound thesis wrong and we’ll close the position down (win or lose) to protect against any bigger losses.

Learn more about Sean at AllStarCharts.com.