The year of the rotation continues as the signs are pointing to changing sector leadership, says Lucas Downey of Mapsignals.com.

Volatility has been the name of the game in 2022. Comfortable portfolios eventually end up uncomfortable. The bear market has come for just about all areas of the market. The latest culprit has been Energy stocks. The recent bellwether for the market has come under immense pressure.

Likely, the drop in commodity prices will help ease inflation and some of the pain consumers feel at the pump. If that’s the case, this latest shift could indicate there’s room for other groups to take the helm.

As I’ll show you, that’s what the data’s pointing to.

Changing Sector Leadership

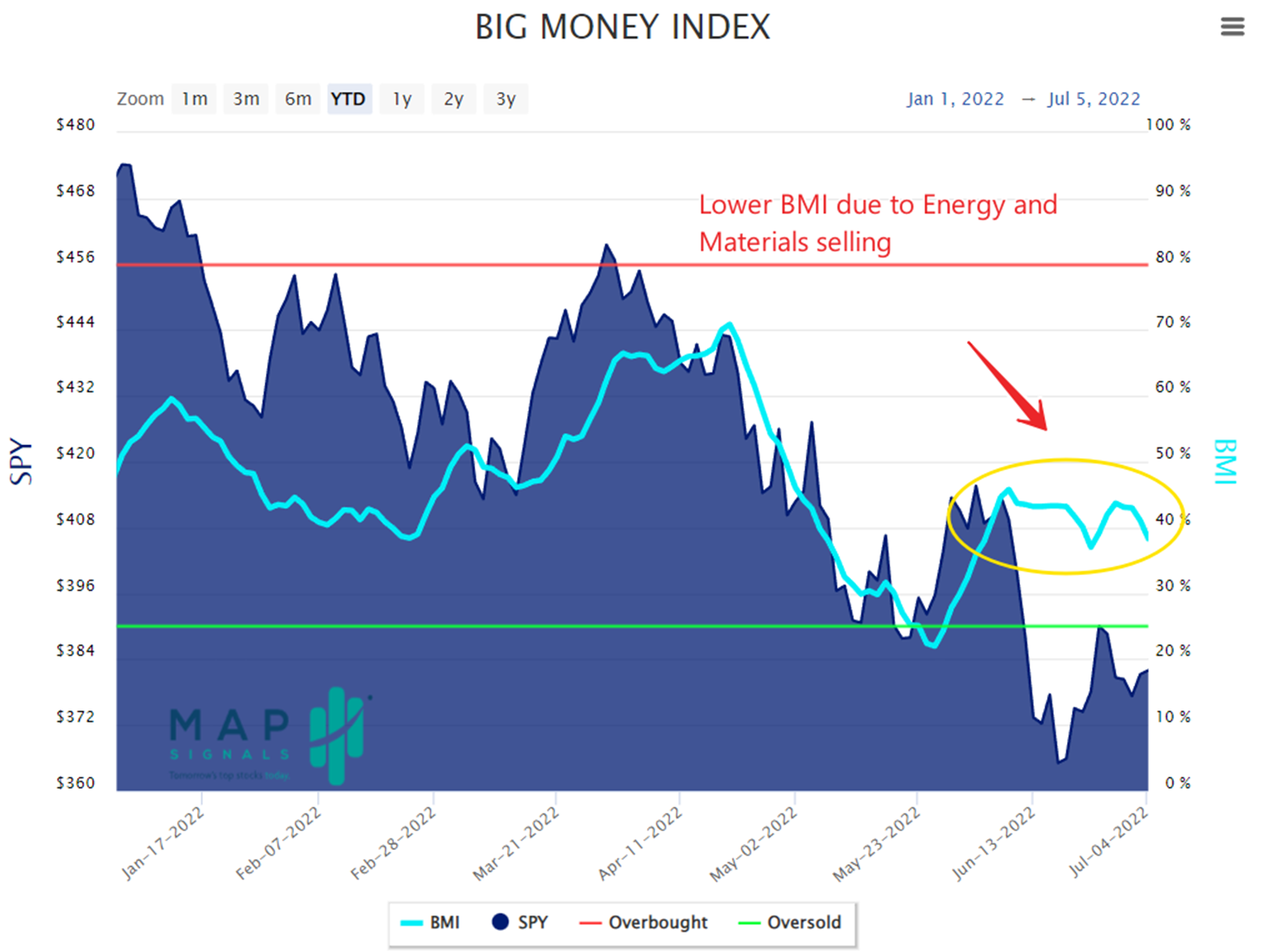

Let’s start from the top. Our data has been very quiet in recent weeks. Much of that is due to rangebound action in markets and typically lighter volumes found in Summer.

However, the Big Money Index is slated to fall as selling has picked up again. This morning’s reading has the BMI at 35%:

Assuming buying remains low, the BMI could remain under pressure. But it’s interesting where the pain is for the market. Much of the red is concentrated in prior leading groups like Energy (XLE) and Materials (XLB).

As I shared last week, the Energy sector has been the only bright area this year with a (then) gain of 39% YTD. As I write this, it’s now at 28%. Money has been pouring out of the group…even this week.

Demand fears have hit commodity-related equities across the board.

Check out how vicious the Energy pullback has been. Beginning June 13 there’s been virtually no buys in the group. Prior to that, the Big Money was flowing hard into the group.

On Tuesday, 40% of our energy universe was sold. That’s an extreme risk-off. See below in our Energy Sector Buy & Sell chart:

As ugly as that selling is, chances are that some macro headwinds can ease, i.e. inflation. Lower fuel and energy costs will strengthen consumers' pocketbooks.

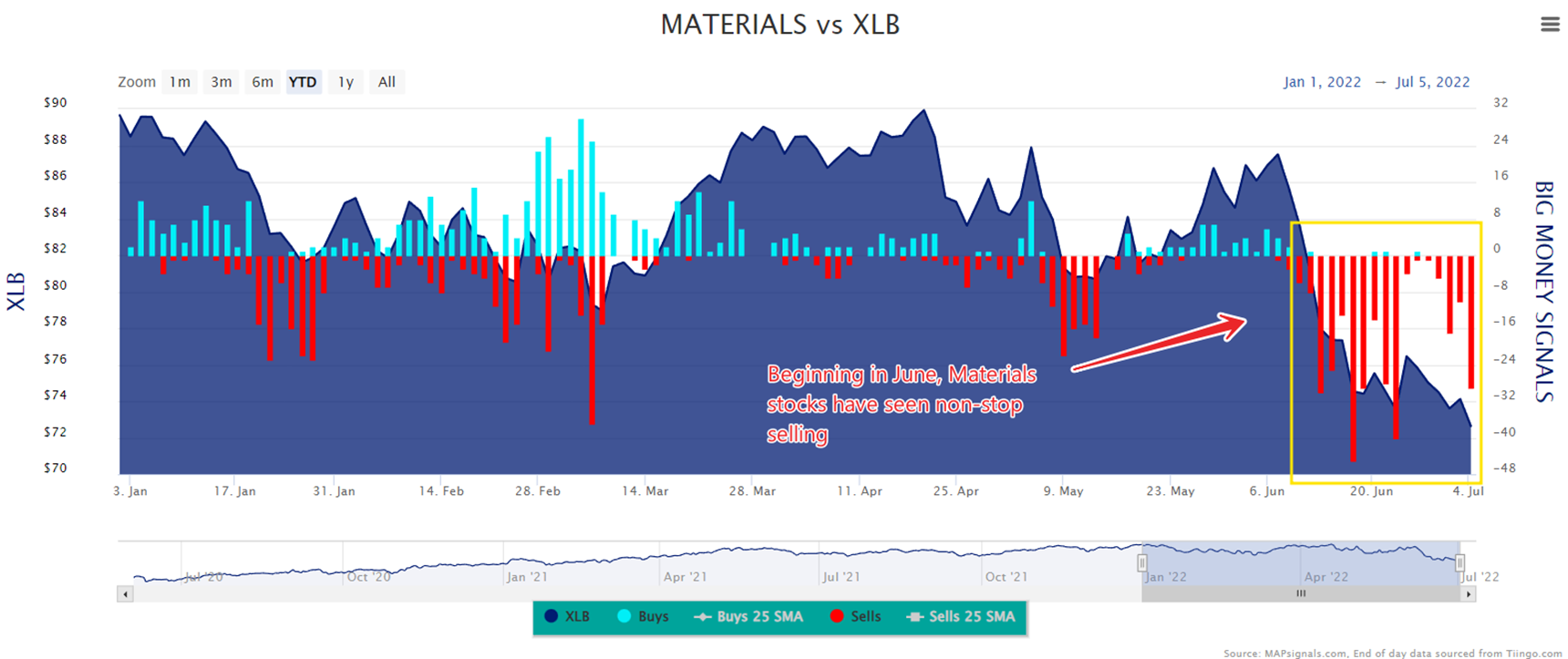

And it’s not just Energy getting crushed, Materials names are reeling too. On June sixth nearly 30% of our Materials universe was sold:

So, what we have are the prior leaders taking a backseat. Oil & Gas, fertilizer, shippers, and steel names are all on fire-sale. And after a brush fire, new life can emerge. Slowly our data appears to be getting more constructive across the board.

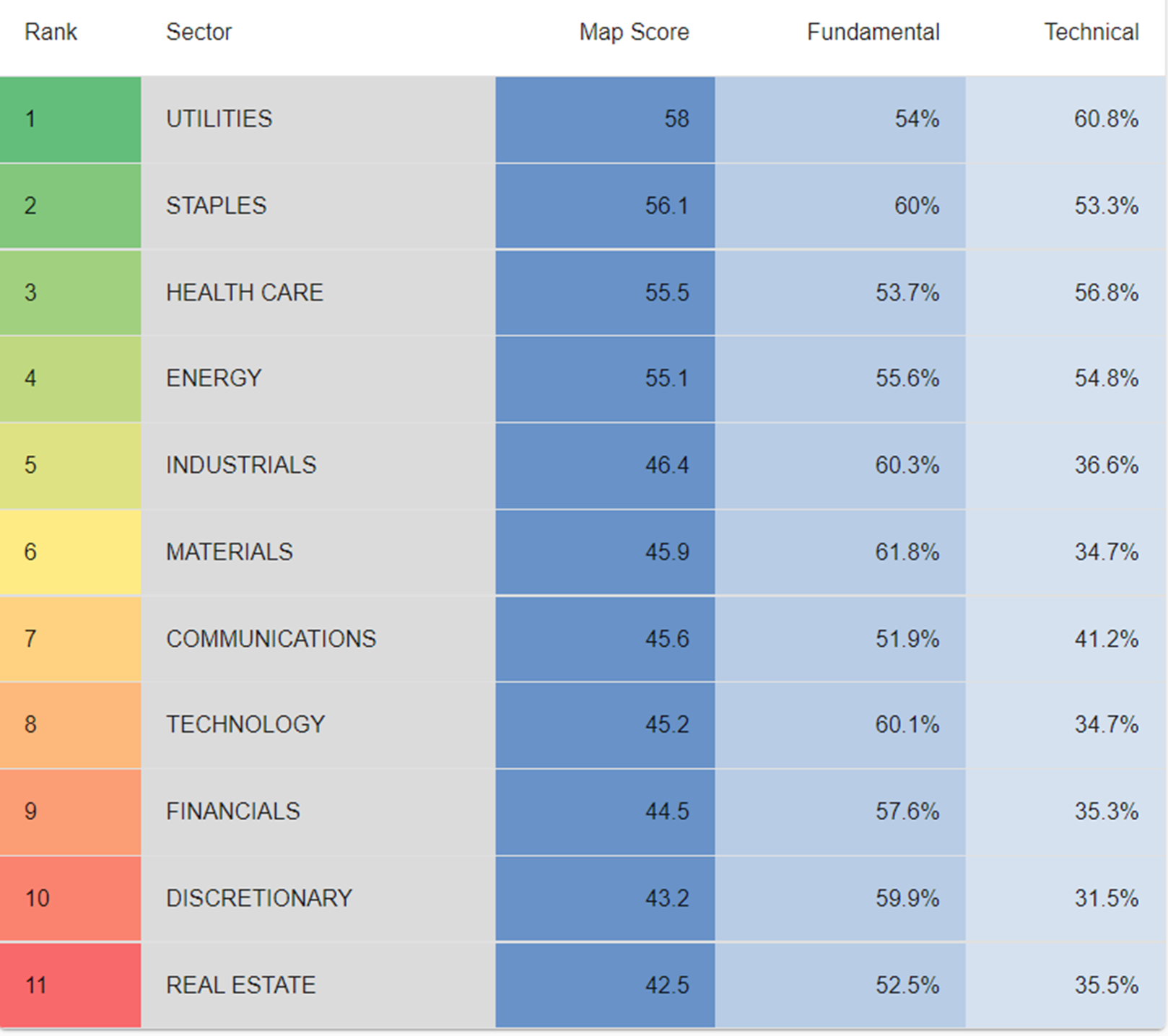

And a great way to visualize this is via our sector ranks. As of Wednesday, Energy has fallen to fourth place behind Utilities (XLU), Staples (XLP), and Healthcare (XLV). Keep in mind, Energy has been the top-ranked area of the market for many months.

When the leader falls, it means money can flow into other areas. From a Big Money buying standpoint, small signs of green are showing up in Staples and Health Care names. Recession fears have driven money into those defensive groups.

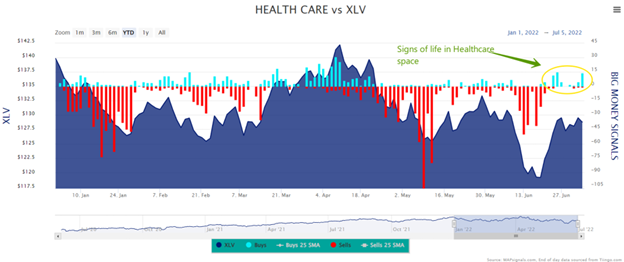

On June 6th, nearly 6% of our Healthcare universe saw buyers:

Recently, Health insurers and Biotech firms are pressing higher. That’s the start of changing sector leadership.

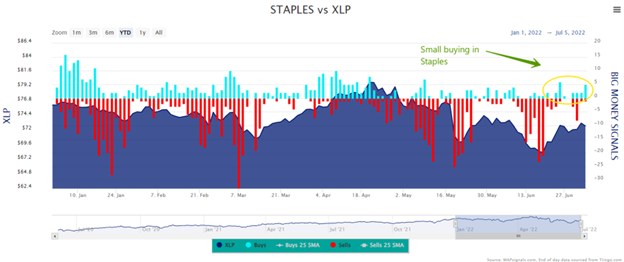

Now let’s peek at the Staples group. There’s a small awakening there too:

And it’s not just the old-school dividend names forging new higher ground, a few growth names are producing buy signals. On the margin, this is very constructive for stocks.

Now I can’t say that the all-clear signal is here for markets. I’ll need to see more convincing data flow through. But at the very least, the risk-off action in commodities does suggest a theme change could be underway.

My bet is we’ll need more clarity on the inflation front before Big Money flows into a group with authority. But I’ll take any positive signs these days

Let’s Wrap Up:

Here’s the bottom line: Energy stocks were prior darlings. Now, they’re falling in rank as selling engulfs the space. Commodity groups are the pain point for the Big Money Index recently.

As painful as that is, it does potentially pave the way for changing sector leadership: Defensive areas like Healthcare and Staples lead the recent green shoots.

Keep in mind, that buying is still light, i.e. low-conviction. But if the last year has taught us anything, it’s that narratives can change quickly.

To learn more about Lucas Downey, visit Mapsignals.com.