Back in the day when I was working as a broker at Bear Stearns in San Francisco in 1989—and well before the fall of that storied Wall Street firm—every morning before the market opened, the entire trading floor would gather at 6:00 am to have a pre-market strategy meeting about what to trade long or short, explains Bryan Perry, editor of Cash Machine.

If you spoke up from among the 100 or so brokers and traders gathered, it was typically from the standpoint of what to buy, and everyone would take a casual note amid a lot of side chatter. However, when someone spoke up about a new short idea, the place went silent.

This is what made Bear Stearns a special place, at least then. A core short was what differentiated the long-only firms from those that trade both sides of the market.

Rising Odds of Recession in Europe: Fear vs Greed

As an emotion, fear is way more powerful than greed, and thus when a highly credible downside investment proposition comes along that looks like a micro or macro shorting opportunity, investors should pay attention. Remember Blockbuster Video, the ultimate casket company? One of the brokers I sat near on the trading floor had a massive short position in BBI as he sniffed out that hanging out at the store to shop for DVDs was about to go by the way of the dodo bird.

To make a long story short, the broker we called “The Hall,” crushed it for his clients. The stock collapsed and tanked from $30 to 30 cents per share. I can think of a number of terminal shorts that have made millions for those that did their due diligence when a disruptive force enters a market sector, or a grand experiment goes bad.

Another example of a stellar short trade was when the Nikkei (N225) was at 40,000 and the Japanese were buying up everything in the United States, from Pebble Beach Country Club to the Time Warner Building in Manhattan. Solomon Brothers came to the market with a three-year term Nikkei put that was unit priced at $3 per share. Bear Stearns was a big player in the selling group. We stood outside the door of the syndicate manager’s office bribing her with trips to Hawaii for allocation. Long story short, it was a seven-ten bagger for those that held.

Rising Odds of Recession in Europe: Is a Financial Storm Coming

To this point, I wanted to bring into focus the Category Five financial hurricane that the European Union (EU) is facing. Shockwaves were felt around the world in financial circles when JPMorgan Chase & Co. CEO Jamie Dimon stated “brace yourself for an economic hurricane caused by the Fed and the Ukraine war.”

Following a 50% rebound of the year-to-date losses for the S&P 500, these words spoken in early June have fallen on deaf ears. But Dimon isn’t the CEO of the most prominent bank in the world because he is careless with his words. What is taking place in Europe, as an economy, in terms of energy inflation, currency destruction, sovereign debt risk, and a leadership vacuum is telling.

To use the phrase, whistling by the graveyard, might be a bit extreme, but it’s probably not far from the reality of what is about to hit the third-largest economy in the world. Soaring energy prices brought on by the cutting off of natural gas supplies from Russia, in combination with record drought conditions, are pushing Europe to the edge.

German baseload power prices are now up five-fold from a year ago to $445/megawatt hour, with little if any relief in sight. Power prices are heavily influenced by the cost of natural gas, which has more than quadrupled. Low wind speeds and high temperatures have reduced wind power generation. Falling water levels in the Rhine and other key rivers and water basins are curbing hydroelectric power output and disrupting the cooling of nuclear reactors to where 50% of France’s nuclear capacity is now offline due to what the government states as “maintenance.”

The eurozone has now found itself in a precarious position of both a hyper-energy crisis, a crumbling common currency, and the rising probability of recessionary pressures that could bring that region to its economic knees. The government of Spain has already outlawed the use of air conditioning in all public places if the temperature outside is under 80 degrees. Does this mean that heating public spaces when the temperature in winter is above 50 degrees will also be banned? This is the stuff of civil unrest not yet unleashed, but could well be soon.

I was listening to a Bloomberg radio interview with the German energy state secretary that opined about how the EU viewed a majority-dependent deal for natural gas with Russia back in the 1990s as a good neighbor, fence-mending, progressive plan to bring Russia into the mindset of a greater, more united Europe. And then Vladimir Putin gained power and decided to reclaim Mother Russia, leaving Europe totally vulnerable to the Russian natural gas umbilical cord.

There are some very basic components to a major economy surviving and thriving, and for the most part, in my view, Europe has it wrong, by a country mile. While there are some beautiful places, fine wine, and cheese to experience, the current EU economy looks like the rearranging of deck chairs on the Titanic. And this is why I believe the US bond market yield is inverted.

The woes of Europe, China’s massive property meltdown and capital flight, coupled with Japan’s eye-popping 260% debt-to-GDP ratio and regressive social structure, all add up to why the United States remains the de facto investment market for oceans of global liquidity seeking a strong currency and stable economy for investing.

Because the US market has rallied, it has a pulling-up effect on all other markets, even if underlying fundamentals are deteriorating. This would be true about the European stock market which has rallied about 10% off its June low, in tandem with the S&P 500. I believe there will be a serious decoupling of the Europe, China, and Japan markets from the summer rally momentum led by the US market.

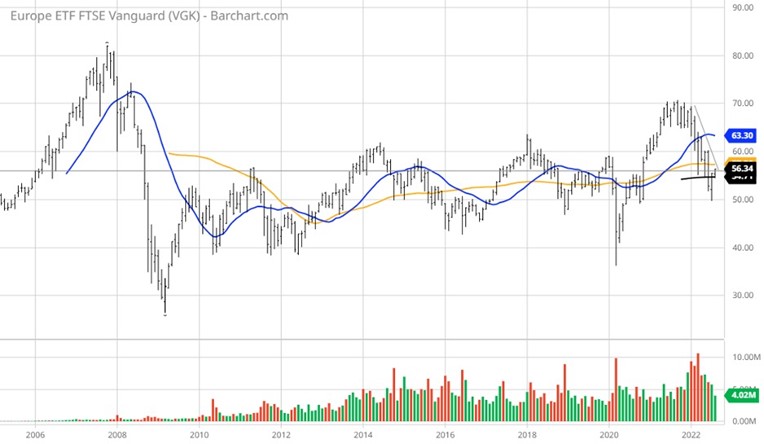

A view of the one-year chart of the most widely traded European exchange-traded fund (ETF), Vanguard FTSE Europe ETF (VGK), which holds stocks from Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, and the United Kingdom, fails to impress.

As shares of VGK show a nice rally off the reaction low in June, going out 15 years (not a typo), this investment has been dead money. Such is true for Japan and China, as well as when pulling up the all-data charts. Roughly 90% of all new innovation is born and nurtured in the capitalist-centric US economy. As an investor seeking a true return on equity…never forget this point. Money never sleeps, and neither should our portfolios.

That short-term surge in shares of VGK was due to world-record sums of central bank quantitative easing (QE) thrown at what history will cite as a series of extremely poor decisions made by a very shallow bench of fiscal leadership. The result could be a real economic decline for greater Europe and likely trigger a full about-face to restarting QE as a crisis management strategy to stave off social calamity.

If shares of VGK break $50 to the downside, then the vigilante pools of global capital will look to break this market. If so, the US market will struggle to trade up on its own with Europe in the tank. Not a prediction. Just an outside observation.