Two inflation reports were released last week. Both indicated that pricing pressures are retreating from peaks – but inflation remains above the Fed’s target of 2%. Progress to that level may be harder to achieve in the months ahead, opines John Eade, president of Argus Research.

According to the latest Consumer Price Index (CPI) report, the overall inflation rate in January of 3.1% was lower than the prior month’s 3.4%. That’s great – except Wall Street was looking for 2.9%.

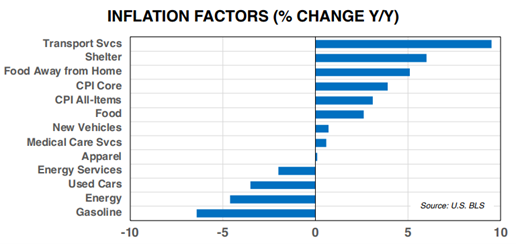

The core CPI rate, excluding food and energy, didn’t move at all and remains at 3.4%. What’s propping up core CPI? Transportation Services (+9.5% YOY) and Shelter (+6.0%). These categories have prices that don’t typically fall sharply.

The other inflation report last week was the Producer Price Index (PPI). It measures pricing trends farther up the supply chain, at the manufacturing level.

Here, we also saw a slowdown in the rate of decline in inflation. The core final demand PPI rate for January was 2.6%, steady month-to-month after having fallen from 4.4% a year ago. We have noted for months that progress will be slow for inflation returning to the 2% level. And nothing was terribly alarming in either report.

Energy prices remain under control, and prices at the PPI Intermediate demand level (even farther up the value chain) continue to outright decline. We think the June 2022 CPI rate was the peak reading for the index this cycle, as the housing market cools, supplies of new vehicles are replenished, and the price of oil stays below $90 per barrel.

The Fed lifted the fed fund rate from 0% to above 5.25% over the past 18 months, and the hikes appear to be reducing inflationary pressures. We still look for the US central bank to be lowering rates in H2 24 as their concern shifts more toward economic growth.