Nell Sloane reports today in her weekly Trading Notebook: records for Apple, SPX. VIX sinks. Fidelity’s no-fee funds. Ace is the place. Treasury borrowing $1.33 trillion for the entire year. Beer jumps in price. Why Corona serves lime. Stay thirsty, my friends.

On Friday we saw the equity markets first head fake only to be driven higher after NFP printed 157k and unemployment fell 0.1 to 3.9%.

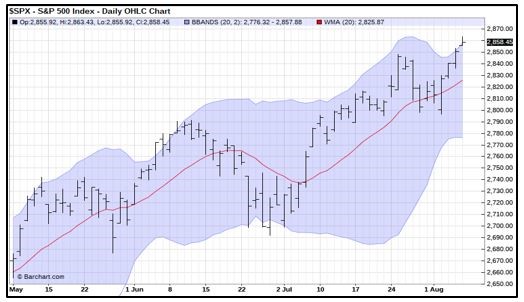

In the morning, the S&P 500 saw initial buying then fell back to 2828 support and then never really looked back, here is the chart from Friday, August 3:

Of course, the day prior was all Apple (AAPL) as their stock rose 3% pushing it finally above the all-important $207 level and more importantly over the $1 trillion market valuation level.

When we look at the S&P 500 (SPX) Wednesday we can see this obvious buy program continuation, we certainly think 2856 is key for the bulls here:

Moving along we can see that the SPX continues to defy gravity and is now firmly entrenched and longer-term bulls can continue to breathe a sigh of relief as the market is well above the 2830 level for now:

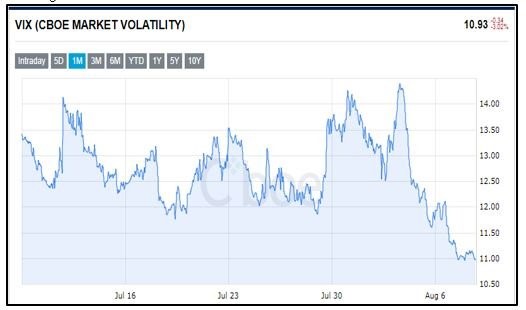

The VIX continues to sink (obviously), falling once again below 11, but we are cautiously awaiting a pop in the VIX complex as the market is driven higher, indicating to us the SKEW is being reluctantly driven in a mass reach for fear of missing out.

This happened on the way up to the January highs and we no doubt feel the linear algo based buy programs will be enticed once again!

**

We know these equity markets are resilient, death defying, but what does it all say about the real driver of nominal asset prices? In plain English, what does it say about the Federal Reserve and how they execute their mandates?

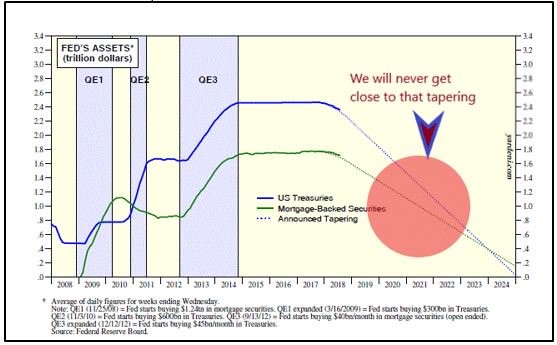

The Fed left rates alone last week in an obvious, trader lite August session, but this following chart made us smirk a bit and we annotated the chart to express our opinion. Yardeni Research puts out some good stuff you should check them out, our annotation is obvious:

Does any investor truly feel that the Fed can actually taper per this indicative slope? We sure don’t but it makes for a good visual. The monetary largesse does have some obvious upsides, like upbeat and ever constant earnings growth, such as this quarter’s 23.5% quarterly profit growth some 2.5x revenue growth over the same period. (Reuters)

**

Locally Ace Hardware is doing their job, the Oak Brook IL based company has opened 87 new stores, creating some 1300 new jobs, with the firm expecting to open 160 total new stores this year. (WSJ)

**

Earnings surprise? Also, it shouldn’t be a surprise as to what sector led this quarter, considering the huge jump in oil this year S&P 500 Q2 earnings growth in the sector was up a staggering 124.9% YoY (WSJ).

**

Fidelity cuts: With all this equity land euphoria, Fidelity felt it was time to add a little bit of deflation to the industry.

In economics when an industry has a general understanding, perhaps even if it’s just a tacit one, when one of its members falls out of line, it can set off a chain of rapid matching cost cutting events.

Now we don’t disagree with their motives, but this is surely a symptom of central banks QE and subsequent no pull back market linear growth structure.

This practice of no fee funds would be impossible in a volatile market, but an obvious possibility in one that simply rises in perpetuity. What this tells us is that complacency has certainly reached a crescendo and this market’s run is well, long overdue by nearly all metrics.

We wish them luck and await the TD Ameritrade, Schwab response to these cost-cutting measures.

**

In other news the DOJ continues to press the AT&T (T) and Time Warner (TWX) merger in the appeals courts. We applaud their efforts as monopolistic practices are predatory in nature, well at least one can argue they are, but economic supply/demand curves can easily postulate this position, price setter or price taker, we know the truth, so we wish the DOJ luck.

As consolidation runs rampant, we figure that department will see some growth in the years ahead! Amazon (AMZN) anyone…just sayin…

**

Bond debt: As for the rest of this week, well the U.S. bond market is swallowing a hefty supply of debt. This week alone will see some $174 billion in new debt, with the big 10-year and 30-year auctions Wednesday and Thursday.

Set ups and concessions have begun, and we should see higher coupons from the May issues. We are potentially looking at possible 3.0% and 3.125% coupon rates respectively, which would put them about an 1/8 or 12.5 basis points higher than May coupons.

**

The U.S. Treasury will borrow some $329 billion this quarter up 21% from their estimates earlier this year and with another expected $440 billion in the final quarter that puts the total upward of $1.33 trillion for the entire year!

Now add an estimated $833 billion federal budget deficit and well, you get a better picture of the Federal Reserve’s “rock and hard place.”

As 10-year duration equivalent aggregate Treasury future net spec shorts continues to grow, we can only suspect once Thursday’s auction is over, they better hope for a decent tail, or else we suspect yields will crater.

Speaking of yields in the U.S. 30-year let’s have a look shall we:

The moving averages are setting up for a continued rise in yields, although we smell a rat here and will need further confirmation above 3.13 to really get an opinion. A fail back below 3.04 and rest assure the long end shorts will be running with their tails between their legs!

**

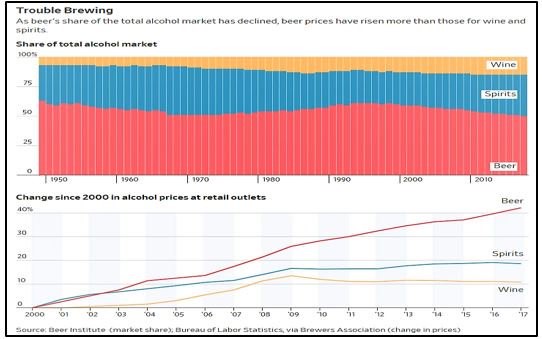

We have been reading a lot about the beer industry lately, all the consolidation, all the microbrews, the ever-changing consumer demand. For the first time according to the Beer Institute (yes, there is such a thing) drinkers chose beer just 49.7% of the time last year. That is down from 60.8% in the mid-90s, with the millennials posting an even greater decline.

The consolidation, the vertical and horizonal integration has been massive.

We remember the AB InBev struggle to acquire then Grupo Modelo, who was kicking their butts with Corona. The $20 billion merger was under fire from the DOJ, but concessions were made and in what was to be nothing more than sleight of hand as InBev was required to give Constellation Brands US brand rights, but it owned the breweries.

Anyway, we can’t help but think the rise in beer prices isn’t going to make up for their lost margins as consumers simply will not pay and will go right to the substitutes of wine and liquor.

Here is a nice chart and you can see, their prices will have to fall, the pricing power is over, in our opinion:

Ok, that does it, we are thirsty now, so we must end this note.

Here’s a bit of knowledge before we go and since we are on the Corona topic, do you know why they serve them with a lime?

It was originally used not as a flavor enhancer, but to keep the flies out! So now you can impress your next bar mate, just make sure you credit the source as we always strive to keep you running, well ahead of the (6) pack, Cheers!

Cheers,

Nell

Subscribe to Nell Sloane's free Unique Insights and CryptoCorner newsletters here