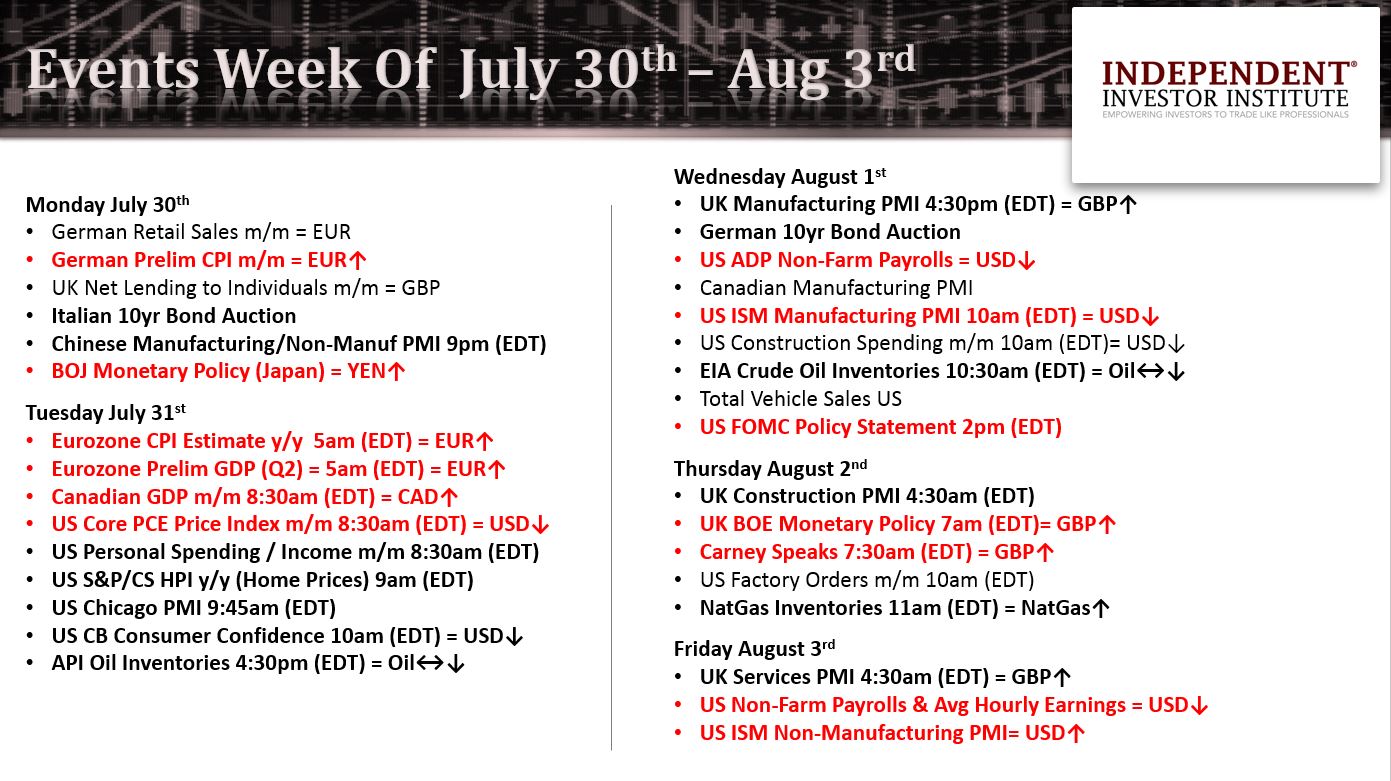

The week-ahead is all about monetary policy (US, BOJ, UK), continued pricing-in of back-half growth risks, and whether the biggest global consumer is being paid more or not (US Jobs report Friday August 3), writes Ziad Jasani over the weekend from Toronto.

View my weekly strategy session video here.

Recorded: July 27, 2018.

Duration: 1:56:55.

We enter the week with Equities in swing-high formations pointed down toward up-trend formations in North America, while relative performance analytics continue to suggest up-trends are likely to hold.

We are effectively hunting for the next macro market swing low for Equities in the week ahead to buy into but we must patiently wait for a sing low formation supported by Bond, Currency & ideally Commodity markets.

Global bond markets are telling us we should still prepare for a few days of Equity-Market negativity, but outside of a break-out of the current basing zone Global-Bonds are in, we can expect Equities to bounce shortly.

Commodity markets are telling us there is certainly a “concern” about back half growth, especially since the Global Commodity Index (DBC) broke down from its up-trend channel on July 11.

However, Oil’s chart technically suggests a consolidation pattern is more likely to play out (short-to-mid-term), between $65 to $75 vs. a wholesale break-down, which in turn supports a bounce for Equities vs. moving into a correction akin to January 2018.

We must note that Oil inventories this week are more likely to hinder vs. help Oil.

Currency markets continue to suggest a stronger USD over the next few months, which can act as a head-wind to both Commodities & Equities. However, into next week we have an indeterminate chart on the USD (UUP). oversold short-term, but dislocated and expensive on annual routines all couched in a consolidation pattern since June 15, 2018.

Furthermore, the EUR/USD pair presents in a basing pattern with short-term direction tilted up (stronger euro, weaker USD). As we see prints of Eurozone CPI & GDP (July 31), US Core PCE Price Index (July 31) and hear from the FOMC on August 1 we’re likely to have more clarity of the next move for the USD in the short-term, which in turn will inform our decisions on Precious Metals, Base Metals, the TSX and Equities at large.

Equity Markets outside of North America remain dislocated and cheap on annual routines relative to the Global Equity Market (ACWX).

For Global-Equity-Markets (ACWI) to stage a bounce in the week or two ahead, participation from the Eurozone Far East & Australasia (EFA) and Emerging Markets (EEM) would be mandatory. Currently, their charts have all moved into resistance of their respective 50-day moving averages and closed below on Friday, July 27 suggesting a congruent move down for a few days prior to a potential bounce.

Macro considerations from last week:

• Renewed Chinese monetary & fiscal stimulus likely to put a floor under Emerging Market Equities (EEM).

• US – Eurozone deal to avert trade war likely to put floor under DAX ~12,500-12,000.

• US – Canada auto tariffs delayed further = Canadian growth risks lessened

• US Q2 GDP strong at 4.1% however, savings rate up and income growth not accelerating

• US Federal Reserve on path to take 2 more rate hikes this year (Sept. 26, Dec. 19), both priced in and inflation metrics stable = USD more likely to cool-off short-to-mid-term before next leg higher.

North American Equities status

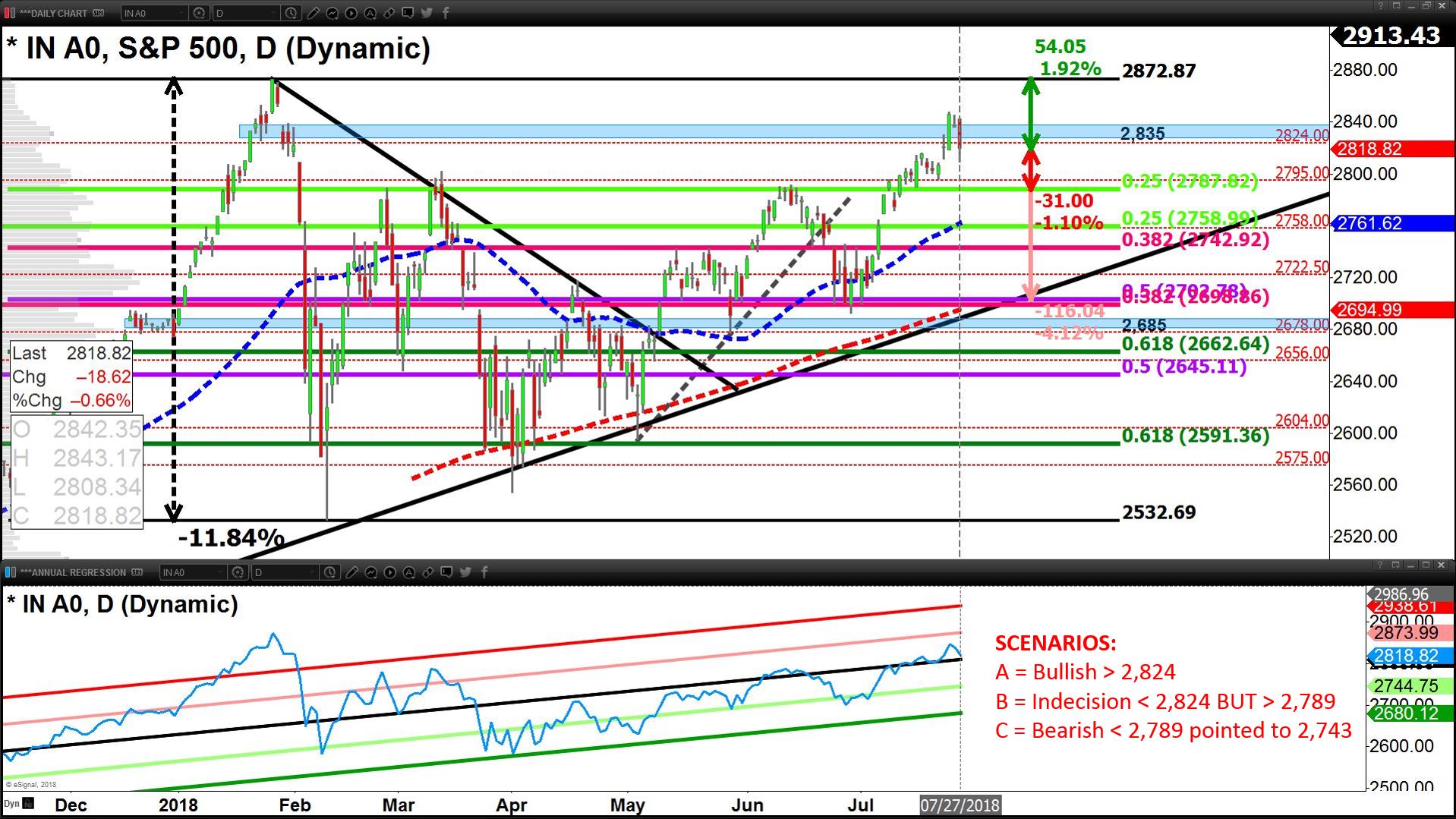

• On Friday July 27, 2018 the S&P 500 (SPX) confirmed a swing high formation cracking down -0.66% and settling below 2,835 at 2,818; theoretically pointed down to support at 2,805-2,788 or -1.1% (Scenario B).

• The VIX Index (Volatility) corroborates continued equity negativity (short-term, days-to-a-week), with risk for VIX to rise towards ~17

• Clear rotation away from growth and towards value within US Equities has taken place (IVW, IVE), suggesting short-to-mid-term fears about growth in the back-half of 2018.

• Key sell-off drivers were Technology (QQQ, XLK, IYW, FNG) and Healthcare (XLV, XHE, XPH, XBI, IBB); both sectors suggest further downside risk of -1.1% to -2.1%).

• Regression & relative performance analytics suggest that sustained negativity unlikely, as most cyclical sectors present as relatively cheap while defensive present as expensive (US Sector Risk-Ladder).

• We could see the S&P 500 re-trace to its 50-day moving average 2,762 before a bounce forms, and must be patient.

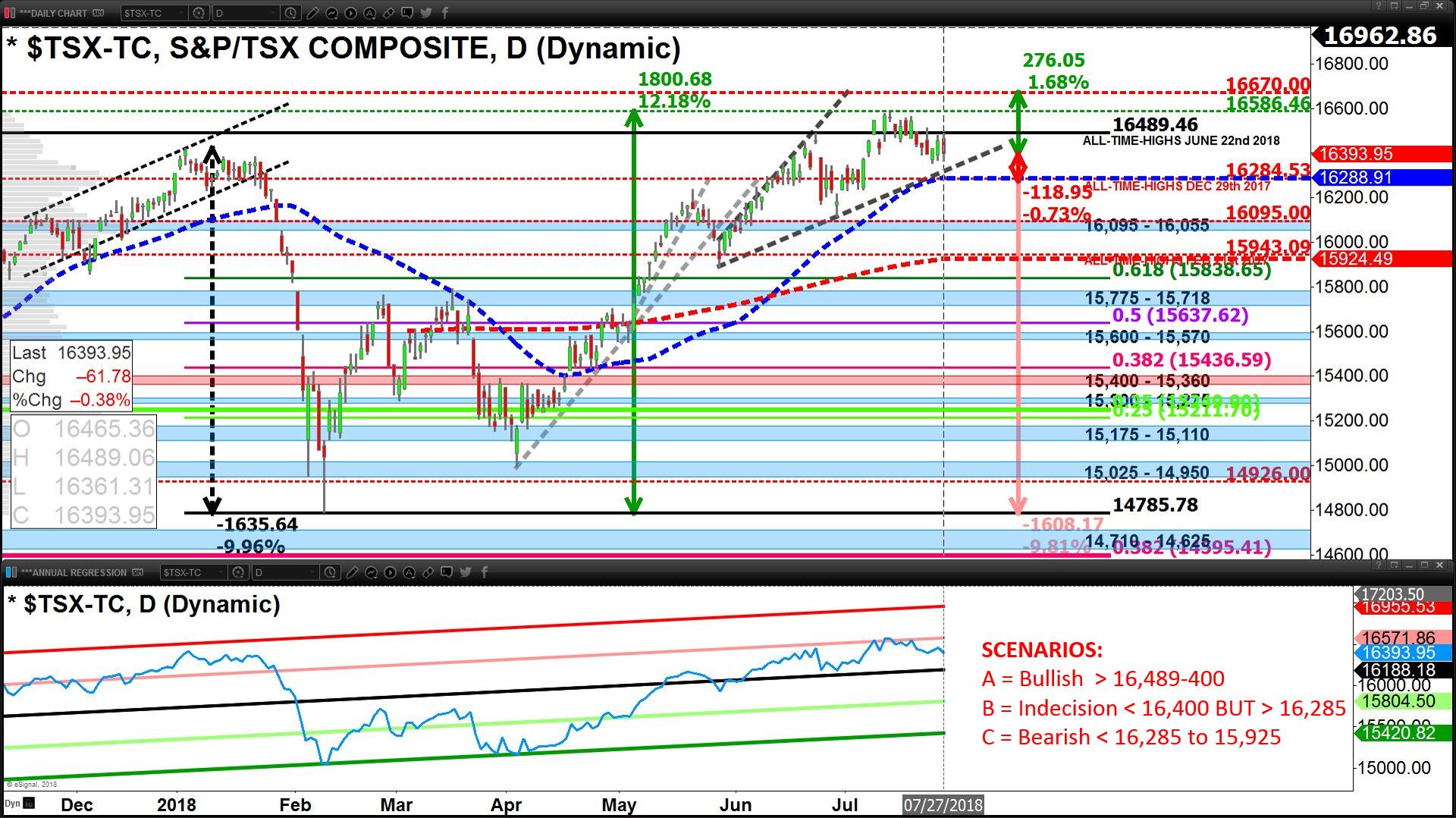

• The TSX is congruently pointed down to its 50-day moving avgerage 16,289 with a better chance for a bounce there.

Strategy for the week ahead

• Enter the week in Defense mode protecting short-to-mid-term swing positions, with some of our trading community members playing out shorts/inverse positions on the Nasdaq (NDQ) & Russell (RUT).

• Wait for a clear swing-low formation on the S&P 500 around support of 2,805-2,788 supported by Bond Markets telling us growth concerns are abating (i.e. swing-high in Government Bond ETFs).

• Corroborate a North-American macro swing-low with the Global-Equity Market (ACWI) participating.

• Focus accumulation for the next macro market swing-low in spaces that present as relatively cheap as depicted by the regression channels on the bottom of all charts following in this report.

• Determine whether Equities can swing-low with or without a weaker USD which will effectively tell us whether Commodity-laden markets/sectors can or cannot participate in the next macro market swing-low for Equities.

• Be open to swing-low trades in Commodities & Currency Markets when direction of the USD is confirmed.

Join Ziad at MoneyShow Toronto Sept. 15 when he discusses Portfolio Management Strategies for Active Investors. Information: ZiadJasani.TorontoMoneyShow.com