The Fed’s quarter point cut failed to inspire stock traders and the lack of a commitment to further easing buoyed the dollar, reports, Adam Button.

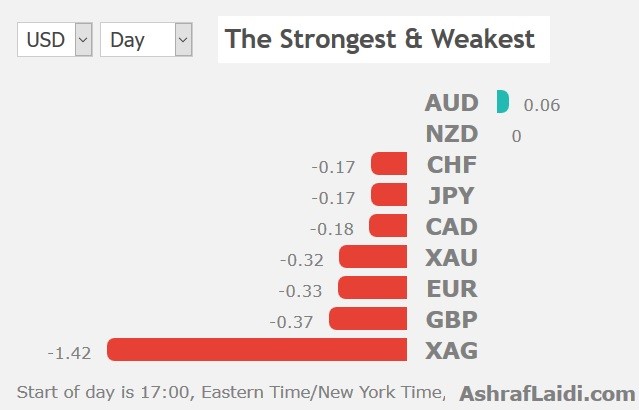

The U.S. Dollar Index jumped after Fed Chair Jerome Powell stunted expectations of a broader Fed commitment to a rate cutting cycle. The dollar was the top performer while the euro lagged, sending the pair to a two-year low. The Bank of England decision is next and expect it to issue the downward GDP revisions, which were signaled early last month. The EURUSD Premium trade was stopped out, while the Dow Jones short hit its final target. Ashraf will publish a video for Premium clients ahead of Friday's jobs report focusing on the central USD view.

The Fed statement was largely unchanged but pointed to global growth and disappointing inflation as the reason for the cut. Fed Presidents Eric Rosengren and Esther George, however, dissented in a sign of disunity on the strategy. The larger market moves came in the press conference when Powell said the cut was to “ensure” growth and that it was a mid-cycle cut. That sent the dollar to fresh highs and cut down the stock market, which sent the US two-year yields as much as 15 basis points above pre-Fed levels.

The market was pricing in a 78% chance of a second cut at the September meeting ahead of the Fed and that has dropped to 64%. It could fall further in the days ahead if other Fed members dial back easing rhetoric. Also, start to watch the U.S. yield curve again. Renewed inversion (as short yields exceed longer term yields) is likely to require fresh easing from the Fed, especially that the fact remains: A negative yield curve has always led to rate cuts (but not always to recessions).

If so, the dollar will continue its rally. EUR/USD broke through 1.11 and the ninth consecutive decline in the Australian dollar. AUD/USD came within a fraction of the 0.6956 June low and that's a key spot to watch in the day ahead.

Onto Jackson Hole

In the day ahead, we will probably get statements from Rosengren and George on their dissents. Other Fed officials may also appear on TV and print to manage the message. Watch for comments from Fed doves in particular, if they also hint at a wait-and-see approach then the market will re-price. The Fed's statement was largely expected, but Powell's press conference contained plenty of verbal stumbles, twists and turns (with regards to the length of easing period & otherwise), leaving us to expect fresh market-moving speeches from Powell in the upcoming weeks and certainly at this month's Fed press conference at Jackson Hole.

The other focus in the day ahead will be the Bank of England. The BOE has a conditional hiking bias based on a smooth Brexit (or some other positive resolution). The consensus is that it will be maintained but there may be hints of a removal. Even in the case of a soft Brexit, it's tough for the BOE to justify a hike while the rest of the world is easing and with Europe struggling. At the same time, they might be hesitant to offer anything that would further damage the pound.

Adam Button is co-owner and managing director of ForexLive.com and a contributor at AshrafLaidi.com. You can see Ashraf’s daily analysis at www.AshrafLaidi.com and sign up for the Premium Insights. Ashraf's Tweet on indices here.