With the S&P up over 100% in the past 13 months, it starts to warp one's expectations for the stock price actions. Meaning that the seemingly nasty sell-off this week is NOT really that nasty in the grand scheme of things, says Steve Reitmeister, editor of Reitmeister Total Return.

Even in the most bullish of years the market will go down on 40% of the days. And sometimes those negative days get stacked together to make 3-5% pullbacks or even 10%+ corrections. But that doesn't change the fact that it’s still very much a bull market.

With that in mind, let's dive into the rest of this week's market commentary.

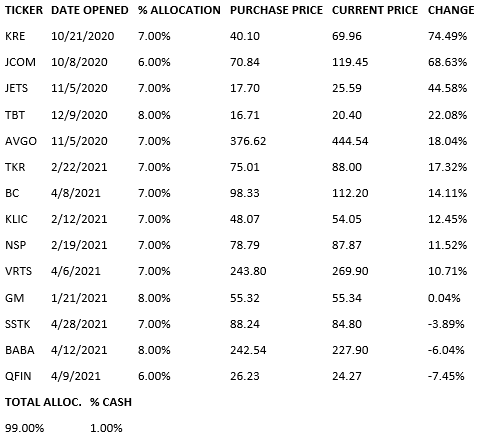

Current Portfolio Holdings

Last Friday my commentary spoke about the market doing the “Hokey Pokey.” In essence, the market had a pretty strong April rallying up more than 5% to a new high at 4,218. And now it is time to take a rest.

So yes, 4,200 will prove to be a spot of resistance followed by some combination of pullback, consolidation, sector rotation. Or in other words...VOLATILITY.

We have seen this 1001 times before. And we will see it 1001 times more in the future. The point being this is the natural way of the market.

Rally > Resistance > Consolidation/Sector Rotation (aka volatility) > Build Energy to Break Out to New Highs.

Reity, why are you so confident this time isn’t different?

First, it is rarely different. And when it is you will see greater bearish catalysts at play.

Second, because I have been investing for 40 years so I have seen this 4004 times or more.

Third, low interest rates still make stocks 2.5X more attractive than bonds. (really...this is the biggest reason making it fairly unnecessary to continue the conversation...but we shall lock this lesson into place). Fourth, coming off yet another strong earnings season.

Fifth, economic data continues to show improvement across the board. I have detailed this week by week in commentary. And most recently you have another strong monthly ISM Manufacturing report. No doubt ISM Services and Employment reports later this week will continue to point to continued economic expansion.

Sixth, the coronavirus #s in the US are dropping as vaccine adoption is well ahead of pace.

Seventh, Biden’s State of the Union address was filled with lots of items that would spark economic growth. This is not Steve Reitmeister, or other Wall Street experts, agreeing that these are the RIGHT policies. It is simply a clear-eyed view that the government checkbook is WIDE OPEN, which is stimulative to the economy > corporate earnings > share prices.

There is no reason to go beyond this point because the above is plenty good enough. So, our game plan is to keep our calm and act like we have been there before (cuz we have ;-)

This will allow us to not get shaken out of our quality stocks during this volatile period. Instead, we will hang on with great confidence that they will rebound with gusto when the next bull run emerges. And if any great buy the dip opportunity emerges, then we will quickly take action.

Now let’s move on to our...

Portfolio Update

Continue on with some additional updates on our positions noted below.

Timken (TKR): You cannot ask for better than what they delivered last Wednesday. It was an impressive beat on the top and bottom line. More importantly they raised guidance for the year ahead. This sparked a parade of analyst love letters propelling shares +3.6% right after the report. That party continued today when most of the rest of our positions were battered and bruised. Not only were estimates raised for this year. Gladly analysts see the good times going into 2022 and beyond. Our +17% gain in shares to date is a nice start. I imagine multiplying that gain by two or three before all is said and done.

Virtus Investment Partners (VRTS): This is just as impressive of an earnings report as TKR. In fact, it might even be a touch better because earnings estimates have come up by about 10% for both this year and next. This explains the initial +4.4% surge right after the report. Yet with estimates so much higher and a fresh street high target of $400 on the books from the 5-star analyst at Piper Sandler, then we can kick back and relax with great expectations of more upside to come.

Brunswick (BC): These guys made it three in a row this earnings season with another impressive beat and raise. This explains why analysts were rushing to upgrade the stock prior to the announcement as their channel checks likely pointed to exceptional results. So a 50%+ earnings beat is nice. But even better is the significantly raised guidance for the future as they expect the good times to continue to roll. This catalyst helped shares cut through the waves of red in the market to end up with a healthy green arrow. Oh, it won’t always be this easy with BC. Yet with shares worth $125+ after this report we can calmly stay afloat in BC a good while longer.

Insperity (NSP): Indeed, NSP makes it four out of four in the win column this earnings season. This may not be so readily evident by the -0.89% showing Tuesday. First, remember how much it ran up into this earnings report. So, a little profit taking is to be expected (under the banner of “buy the rumor, sell the news”).

Yet make no mistake about it. This report was an ample beat and raise that already has one analyst pounding the table with a fresh $103 target on shares. In particular, he notes the obvious acceleration in business that should continue to pick up speed. I suspect NSP will be knocking on the door of that $103 target coming into the next quarterly earnings report.

Shorting Treasury Bonds (TBT): The Fed did the expected at their 4/28 meeting, which was to make no waves. However, they do point to an improving economy and inflationary pressures building. That is likely a precursor to them taking their foot off the gas pedal in future meetings. Even before raising rates (which they say they don’t intend to do til 2023...which is a borderline insane statement given how far out in the future that is) they will likely move towards less bond buying on their part (QE) that would also lead to higher rates because less demand for bonds > higher rates. The start of that move would likely be the catalyst to see rates quickly climb a quarter to half a percent in no time.

Let’s take this one step further. One of CNBC’s favorite investment experts is Jim Paulsen. And he recently talked about a 40% chance of runaway inflation in the future. And yes, that would be a big plus for our TBT position (but not so hot for the rest of the economy).

Chinese Stocks After State of the Union (BABA & QFIN): There was some tough talk on our economic relationship with China during last week’s the State of the Union address. Will that lead to stormy relations as we saw back two summers ago with the China trade talks? Or just posturing with no real meat on the bone? Regardless, it is VERY unlikely that any aspect of US/China trade would alter the growth trajectory for these two firms. So, their sell off since last Thursday should likely prove short lived.

General Motors (GM): Why so weak last Thursday? Because of continued industrywide issues noted by Ford on chip shortage and what that means for the outlook for selling cars. On that Ford dropped -9.5% on the day. In that light the 3.3% decline for GM was not so bad.

Remember we never bought GM for the CURRENT outlook. No, it was about the long-term shift to EV that should help inflate the PE and see shares rev up to around $100 or more in next one-two years. So the Ford announcement is not good news...but doesn’t really change the long-term trajectory of why this is still an attractive investment. The best part of all of this is that expectations should be fairly low for GM’s report. If true, then hopefully any ray of hope can lead to a near term pop in shares.

Learn more about Steve Reitmeister at StockNews.com.