A broad range of asset classes are priced for perfection and are particularly vulnerable should the economy show signs of slowing down. I strongly recommend that you start 2018 making sure that you have a risk management plan in place, says Marvin Appel, MD, PhD.

The past five years have been tough for the typical bond investor as the Barclays U.S. Aggregate Bond Index returned just 2%/year in total return. With the yield on that index still at the historically low level of 2.7%, the prospects for investment grade bonds at current interest rates do not appear bright even if interest rates remain stable.

In fact, the Federal Reserve expects to increase short term rates by an additional ¾% in 2018, which would bring them up to 2%-2.25%.

Inflation is threatening to heat up

Commodity prices have jumped, led by a recovery in energy prices after their 2015 rout.

Commodity price inflation is now at its highest level in six years after jumping by the largest amount since we emerged from the severe 2008-2009 recession. (See chart below.)

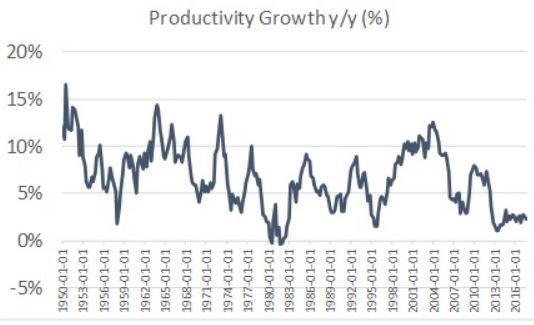

Meanwhile, U.S. businesses and workers are finding it hard to be more productive.

For the past five years, real hourly output has been inching ahead at just 2%/year, the lowest sustained reading since the data began. (See productivity chart below.)

Figure: Trailing 4-quarter change in the productivity of U.S. workers. Productivity growth is at its lowest sustained level since the data began in 1950.

Higher raw materials prices and stagnant productivity have not yet filtered into consumer prices or wages; inflation remains near the 2% Fed target and wages have been growing at approximately 2.5%.

There remains some cushion to delay the onset of higher inflation:

- Capacity utilization remains below 80%.

- The low unemployment rate of 4.1% does not count the significant numbers of potential workers who might yet be coaxed back into the labor force.

As a result, although it does not appear that inflation is an imminent threat for 2018, it will certainly be rising over the next several years.

When inflation does get beyond the Federal Reserve's 2% target on a sustained basis, the Fed will likely respond with more aggressive rate hikes. That will cause the stock and bond markets to stumble.

But in 2018, we appear to remain in a stable environment with interest rates pushing higher at a gradual rate.

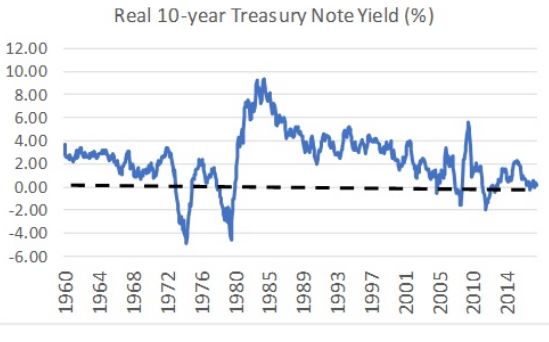

Treasury yields are low relative to inflation

One factor that has predicted future bond performance is the difference between the yield a bond pays and the rate of inflation.

This difference is called the real yield. When real yields are high it means that bonds are relative bargains. Historically, higher real yields have predicted higher returns. Conversely, when real yields are low it means that bonds are relatively overpriced.

Historically, low real yields have predicted below-average subsequent returns. The chart below shows that the real yield on 10-year Treasury notes is close to zero. The only time that real yields were lower than this on a sustained basis was during the runaway inflation of the 1970s. This does not bode well for the returns on investment grade bonds going forward.

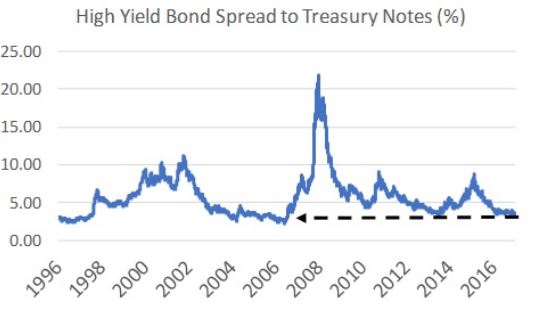

There is no margin of safety for high yield bonds

When investing in high yield bond funds, one measure of whether they are relatively expensive or cheap is the difference between the level of interest that high yield bonds are paying and the level of interest you could get from Treasury notes of the same maturities.

This is called the “yield spread” and is a measure of how much the bond market is charging high yield bond issuers for bearing the risk of default.

The chart below shows the past 22 years of the yield spread between high yield bonds and Treasuries. At 3.4%, it is near an all-time low. This will be acceptable for investors as long as the default rate stays near its current low level of 1.5%. Indeed, the spread stayed in the 3%-4% range for much of 2004 and 2006, which were profitable years for high yield bonds. However, with the spread and with absolute yields so low, there is no margin for error if the business climate deteriorates.

Note: We never recommend buying and holding high yield bond funds because losses can be severe during downturns. This is especially the case now. Rather, you should utilize a timing model to limit losses when the next correction occurs, which we do for our own clients.

Investment implications

As we start 2018, the trends for many risky assets remain up and our models continue to indicate favorable conditions for U.S. and foreign equities and for high yield bond funds. Our investment grade timing model also remains on a buy signal, but potential returns are limited because interest rates are so low.

We recommend investing your full allocation to equities in a mix of large-cap U.S. stocks (e.g.: S&P 500 Index). In addition, some of your equity portfolio can be allocated to a combination of developed country foreign stocks. Like: iShares MSCI EAFE Index ETF (EFA) and emerging markets. Like: iShares MSCI Emerging Markets Index ETF (EEM), or the Vanguard analog, (VWO).

High yield bond funds also remain attractive as we start the year. However, with yields as low as they are, you should pay close attention to risk management. We took some profits in high yield bond funds for our clients, and I would recommend that you consider doing so as well with a fraction (such as 1/3) of your high yield bond holdings.

With the Federal Reserve on track to continue raising short term rates, the best potential fixed-income investment is floating rate bond funds. These funds’ yields rise in tandem with short term rates, so in contrast to funds that hold bonds with fixed coupons, floating rate funds should actually benefit from the Fed’s future rate hikes. As with high yield bond funds, the biggest risk to floating rate funds is a deterioration in the economy.

Bottom line: A broad range of asset classes are priced for perfection and are therefore particularly vulnerable should the economy show signs of slowing down. I strongly recommend that you start 2018 making sure that you have a risk management plan in place, as we do for our own clients.

Subscribe to investment newsletter Systems and Forecasts here…